Buy Kajaria Ceramics Ltd for the Target Rs. 1362 by Motilal Oswal Financial Services Ltd

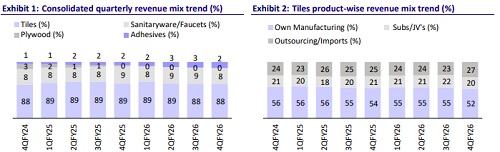

Tiles’ volume/revenue/PAT up 11%/12%/266% YoY in 4Q

* Kajaria Ceramics (KJC) reported a healthy quarter, with an 11-12% YoY rise in tile volume and revenue owing to business unification efforts and reduced competition amid severe gas availability issues in Morbi.

* Overall, revenue/PAT grew 12%/266% YoY (4-7% beat on our estimates).

* Bathware and adhesives’ revenue grew 5% and 92% YoY, respectively.

* While gross margin contracted 165bps YoY, EBITDA margin expanded 786bps YoY to 19.2% on cost optimization efforts and OpLev benefits.

* In FY26, revenue/EBITDA/PAT grew 4%/38%/65% YoY, with an EBITDA margin of 17.9% (up 440bp YoY).

* KJC’s net cash level surged to INR7.9b, aided by tight working capital management.

Key highlights from the management commentary

* Production in 4QFY26 dipped 7% YoY, but sales volume grew 11% YoY, resulting in a high EBITDA margin of 19.2%.

* The demand uptick, which started in Jan’26, has continued until now. Business unification at KJC also helped it achieve healthy growth.

* Large players have gained market share amid severe gas availability issues faced by Morbi-based players. This situation may reverse when Morbi production revives in the coming quarters.

* KJC is confident in maintaining its EBITDA margin in the 18-19% range.

* Morbi players have taken price hikes of 35-40% over the last two months.

* Most of the plants in Morbi were shut in March due to gas unavailability. Some of them, including KJC, started operations from 16th Apr’26, and the remaining are scheduled from 1st May. Inventory levels are below normal at the factory as well as in the channel. KJC outsources 25-30% of tile volume from Morbi-based partners. Thus, sales volume may be slightly affected in 1Q, which is normally a low-volume quarter.

* KJC has announced a share buyback worth INR2.9b at INR1,380 per share.

* It plans to invest INR2.1b in capex at Srikalahasti, AP, by 10msm p.a. from 8.8msm GVT capacity currently, to be commissioned by Mar’27.

Valuation and view

* We raise our earnings estimates by 4% owing to better margin estimates. In line with reviving demand and a healthy 18-19% EBITDA margin guidance, we expect a CAGR of 11%/12%/12%/17% in tiles’ volume/ revenue/EBITDA/PAT over FY26-28 (FY19-26: 6%/7%/10%/13%).

* We also project ~19% RoE, ~26% RoCE (pre-tax), and ~35% RoIC in FY28 and more than INR5b annual FCF for the company.

* The stock has risen ~30% from its lows in Mar’26. Expecting recovery in sales volume, high margins, and strong cash flows, we reiterate our BUY rating on KJC with a TP of INR1,362, based on 30x FY28E EPS.

* Strong comeback by Morbi players may intensify competition and dent the financials of KJC. This remains a key monitorable in the near term.

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041