Buy ICICI Prudential Life Insurance Ltd for the Target Rs 650 by Motilal Oswal Financial Services Ltd

VNB margin expands 250bp YoY; 60bp beat

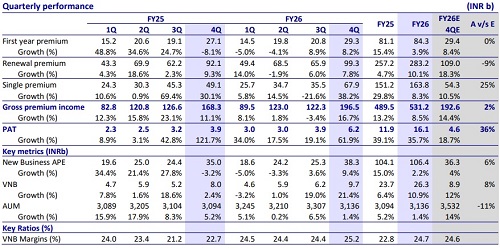

* ICICI Prudential Life Insurance (IPRU) reported APE of INR38.3b (6% beat), reflecting growth of 9% YoY in 4QFY26. For FY26, APE grew 2% YoY to INR106.4b.

* VNB margin for the quarter stood at 25.2% vs our estimate of 24.6% and 22.7% in 4QFY25. Absolute VNB at INR9.7b was 8% above our estimates, growing 21% YoY. For FY26, VNB grew 11% YoY to INR26.3b, leading to a 190bp YoY expansion in VNB margin to 24.7%.

* EV at the end of FY26 was at INR530b, growing 10.5% YoY, with operating RoEV at 11.9% for the year.

* In the long run, management expects to maintain RoEV in the range of 13– 14%, subject to yield curve movements and VNB trajectory.

* We have increased our APE/VNB estimates by 1.8% each for FY27/28, considering the 4QFY26 performance. However, owing to variances in FY26, we have cut our EV estimates by 1.2% each for FY27/28. We reiterate our BUY rating with a TP of INR650 (based on 1.4x FY28E EV).

Protection growth remains strong post GST boost

* IPRU’s gross premium grew 17% YoY to INR196.5b (in-line) in 4QFY26, driven by 8% YoY growth in renewal premium, while single premium grew 38% YoY.

* APE growth of 8% YoY in 4QFY26 was driven by 15% YoY growth in ULIP, 30% YoY growth in protection, and 73% YoY growth in the lumpy group business. Non-par business declined 18% YoY owing to a high base post the launch of a new product in 4QFY25.

* Within the protection segment, the retail business witnessed 60% YoY growth, with its contribution to APE rising from 4.9% in 4QFY25 to 7.2% in 4QFY26, driven by the GST exemption-led boost.

* The 250bp YoY expansion in VNB margin to 25.2% in 4QFY26 was a result of: 1) rise in the contribution of retail protection, and 2) expanding margins of ULIP due to higher sum assured and rise in rider attachments.

* Commission expenses grew 14% YoY to INR18b, while operating expenses grew 57% YoY, resulting in a rise in EoM ratio to 16.4% from 14.7% in 4QFY25. For FY26, the cost ratio increased slightly from 17.7% to 18.1%.

* On the distribution front, agency/direct channels witnessed tepid performance, contributing 23%/12% to the mix, owing to the impact of high base. IPRU is investing in enhancing its tech and analytics capabilities to improve agent productivity, while also adopting a micro-market approach.

* The bancassurance channel witnessed 5% YoY growth, contributing 31.5% to the mix. The corporate agent channel continued to witness strong growth (+18% YoY), contributing 13.4% to the mix (from 12.4% in 4QFY25), with IPRU focusing on expanding partnerships as well as increasing the share of business with existing partners.

* On a premium basis, persistency declined in 4QFY26, with 13th month persistency at 82.1% (84.3% in 4QFY25) and 61st month persistency at 61.2% (61.9% in 4QFY25). However, 37th month persistency improved from 73% in 4QFY25 to 75.4% in 4QFY26.

* AUM grew 1% YoY to INR3.1t, while solvency improved to 227.3% (212.2% in 4QFY25).

* EV was impacted by operating assumption variance of INR2.6b, persistency variance of INR2.6b, and economic assumption variance of INR7.8b. The operating assumption variance was due to the loss of ITC, persistency variance was due to an annuity product, and economic assumption variance was largely debt-driven.

* IPRU’s PAT grew 62% YoY to INR6.2b in 4QFY26 and included an exceptional gain of INR1.1b from 100% stake sale in ICICI Prudential Pension Fund. For FY26, PAT grew 36% YoY to INR16.1b

Highlights from the management commentary

* The strong growth trajectory witnessed post GST exemption continued till Feb’26, with macro conditions impacting growth in Mar’26. Going forward, management aims to adopt a cautious outlook toward growth while focusing on maintaining a granular approach.

* The non-par segment faces challenges as products are benchmarked against bank FD rates, making current offerings relatively less attractive. No pricing changes were undertaken as yield curve movements remained favorable; repricing may be considered once yields soften.

* The company is prepared for the IndAS transition but will seek a one-year forbearance, given the short transition window and pending clarity on certain aspects. Valuation and view

* IPRU’s continued efforts toward the product mix shift and increasing retail protection contribution have resulted in continued YoY expansion in VNB margin, despite the loss of input tax credit after GST exemption. In the long term, the company’s profitability will be supported by higher volumes, driven by GST exemption, increased traction of non-linked products, and improved product-level margins.

* We have increased our APE/VNB estimates by 1.8% each for FY27/28, considering the 4QFY26 performance. However, owing to variances in FY26, we have cut our EV estimates by 1.2% each for FY27/28. We reiterate our BUY rating with a TP of INR650 (based on 1.4x FY28E EV).

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412