2025-10-16 03:16:48 pm | Source: Motilal Oswal Financial Services ltd

Buy ICICI Lombard Ltd for the Target Rs. 2,400 by Motilal Oswal Financial Services Ltd

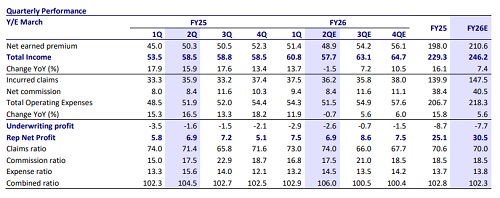

* YoY decline in NEP growth due to 1/n accounting, while recovery is seen in the auto sales.

* The combined ratio increased in 2QFY26, led by higher claims and commission ratios.

* Loss ratios are expected to remain elevated, but operational leverage is likely to aid the opex ratio.

* GST exemption implications and TP motor premium hikes are the key monitorables.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Disclaimer:

The content of this article is for informational purposes only and should not be considered financial or

investment advice. Investments in financial markets are subject to market risks, and past performance is

not indicative of future results. Readers are strongly advised to consult a licensed financial expert or

advisor for tailored advice before making any investment decisions. The data and information presented

in this article may not be accurate, comprehensive, or up-to-date. Readers should not rely solely on the

content of this article for any current or future financial references.

To Read Complete Disclaimer Click Here

Latest News

NCW chief Vijaya Rahatkar highlights importance of M...

Listed debt entities must list transferred unlisted ...

India must reduce dependence on oil: Jayant Sinha

India's first indigenous hydrogen fuel cell train ki...

Biofuel to play key role in India's energy transitio...

Don't make citizens run from pillar to post for serv...

Anupam Kher gifts a special surprise to Satish Kaush...

Sub Jr Women Championship: R K Roy Hockey Academy be...

Sensex may face resistance at 76,300, Nifty support ...

Nine of India's top-10 firms lose Rs 2.74 lakh crore...

More News

Financials Banking Sector Update : Reconciling banking business updates with systemic data b...

Healthcare Monthly Sector Update : Acute/Chronic witness highest YoY growth in 24m By Motilal Oswal Financial Services Ltd

Financials Banking Sector Update : Are there upside risks to FY27E credit growth by Motilal Oswal Financial Services Ltd

Consumer Sector Update : Earnings outlook materially improves for the sector by Motilal Oswal Financial Services Ltd