Buy Hindustan Petroleum Ltd For Target Rs. 500 By Yes Securities Ltd

Core performance in line, inventory losses in refining and marketing along with LPG burden drags profitability

Hindustan Petroleum’s Q3FY25 reported performance showcases in line core refining performance while marketing marginally lower. With an EBITDA of Rs59.7bn and PAT at Rs20.2bn, a subsidy burden of Rs31bn on LPG weakened the reported performance. Reported EBITDA and PAT is lower than our expectations. The reported GRM is of USD6/bbl and Rs6/ltr of blended gross marketing margins, while the core integrated margins stood at USD5.9/bbl. We maintain BUY rating with a revised TP of Rs500 (earlier 475) valuing it on SOTP (core business at 7x EV/EBITDA and investments at Rs113) including Rs47/share from Lubes business.

Result Highlights

* EBITDA/PAT at Rs 59.7/30.2bn is up 1.76x/4.7x YoY and 1.2x/3.8x QoQ. This is lower than ours, we estimated EBITDA/PAT at Rs 72.5/38.8bn, also impacted by higher interest expenses. The integrated margins were down impacted by weaker marketing while GRMs were in line. The marketing segment continues to be impacted by LPG subsidy burden.

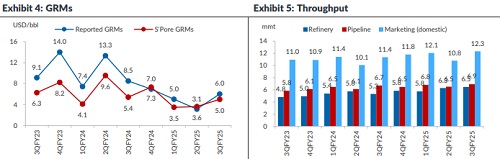

* The reported GRM of USD6.01/bbl in line to ours USD 5.97/bbl (USD3.1 the previous quarter, USD8.5 a year ago), while the Arab heavy-light difference was USD1.9/bbl (USD1.3 in the quarter prior). The core GRM at USD6.9/bbl, (USD4.8 the prior quarter, USD10.7 a year ago), a USD1.9/bbl premium to the benchmark USD5, higher than our estimates with a distillate yield of 75.5% vs 76.5% the last quarter. We calculate USD0.9/bbl refining inventory loss for the quarter (a loss of USD1.7 the prior quarter and USD2.2/bbl a year ago). Refinery throughput was 6.47mmt at 111% utilization (108% the previous quarter, 95% a year ago).

* Integrated core EBITDA margin of USD5.9/bbl (USD3.7 the prior quarter, USD2.6 a year ago) meeting our expectation of USD5.9/bbl. ? Core marketing EBITDA (back-calculated) was Rs3.4/ltr (Rs2.3 the prior quarter, negative Rs0.2 a year back), lower than our expectation of Rs3.9/ltr. Domestic marketing throughput was 12.3mmt, up 8.5% YoY and 14.2% QoQ (vs. the industry’s growth of 4.8% YoY and 7.9% QoQ). Motor spirit sales were 2.5mmt (up 9.2% YoY and 3.8% QoQ), and diesel 5.4mmt, up 4.9% YoY and 19.4% QoQ. Industry motor spirit and diesel sales were up 9.7%/4.8% YoY and 3.5%/18.9% QoQ. The company has a negative buffer for LPG subsidy amounting to Rs 76bn as of end 9MFY25, and Rs 31bn in Q3FY25 pertaining to LPG subsidy. This is in an absence of GOI receivables and the revenue to that extent has not been recognized. Product market shares. Hindustan Petroleum maintained their marginal market share for high-speed diesel and motor spirits at 22.4% and 24.5% respectively. The Rs4.8bn, forex losses impacted the quarterly profitability.

* Capex for 9MFY25 was Rs 95bn (Rs29bn in Q3FY25) and a target of Rs150bn for FY25. Debt of Rs540.2bn was up Rs40.2bn YoY and down Rs116.5bn YoY.

* 9MFY25 performance: EBITDA at Rs 108bn (vs Rs 200.4bn in 9MFY24) while PAT at Rs 40.1bn (vs Rs 118.5bn) and the reported GRM at USD4.7/bbl (vs USD9.8). The core integrated margins were at USD3.9/bbl vs USD6.1/bbl while the marketing EBITDA/ltr (Rs) was at 1.9 vs 2.6 in 9MFY24.

Valuation

At CMP, the stock trades at 8.4/6.8/6.8x FY25e/26e/27e EV/EBITDA and 1.7/1.5/1.4x P/BV (excl. investments, it trades at 6.9/5.6/5.7x FY25e/26e EV/EBITDA and 1.1/1.0/0.9x P/BV). We maintain BUY rating with a revised TP of Rs500 (earlier 475) valuing it on SOTP (core business at 7x EV/EBITDA and investments at Rs113) including Rs47/share from Lubes business.

Please refer disclaimer at https://yesinvest.in/privacy_policy_disclaimers

SEBI Registration number is INZ000185632