Buy Gujarat Gas Ltd for the Target Rs. 490 by Motilal Oswal Financial Services Ltd

Strong Morbi traction, merger emerge as key positives

* Gujarat Gas’ (GUJGA) city gas distribution volumes beat our estimate by 12% at 8.9mmscmd (down 5% YoY). While D-PNG volumes stood 7% below est., CNG volumes were 4% above our est. I&C-PNG volumes came in 26% above estimates at 4.4mmscmd. Gas trading volumes stood at 4.6/4.9mmscmd in 4QFY26/FY26. EBITDA stood at INR7.8b (+34% YoY, -18% QoQ). APAT stood at INR5.7b (+15% YoY, -19% QoQ), as the company incurred exceptional expenses of INR618m in 4Q.

* Things we liked about the result: 1) Morbi ceramic cluster gas consumption ramped up significantly during Mar-May’26 from 0.4mmscmd to ~8mmscmd. Due to the unavailability of alternate fuels, volumes in Morbi can go as high as ~8.9mmscmd. The company expects similar volume in Jun/Jul’26. 2) CNG volumes were up 12% YoY in 4Q, led by strong growth across both Gujarat (+11%) and non-Gujarat geographies (+18%). 3) Due to the merger, tax losses of ~INR19b still remain available for set-off against future profits. 4) Management has guided for gas trading segment EBIT of INR11-12b p.a.

* Key monitorables: 1) GTL is expected to get listed by end-Jul’26. 2) With I&CPNG being supplied under monthly contracts in Morbi currently, volumes remain highly susceptible to declines in alternate fuel prices.

* Valuation and view: The stock (ex-GTL) currently trades at 13.5x FY28E EPS. We reiterate our BUY rating on the stock with an SoTP-based TP of INR490. In our SoTP-based valuation, we value: 1) the city gas distribution segment at 12x FY28E EV/EBITDA (INR261/sh); 2) the gas trading segment at 5x FY28E EV/EBITDA (INR58/sh); 3) add FY28E net cash balance (INR86/sh); 4) the gas transmission business (GTL) at 8x FY28E P/E (INR66/sh); and 5) investment in subsidiaries, associates, and JVs at 0.8x P/B (INR18/sh).

Strong CGD volume performance

* W.e.f. 1st May’26, the GSPC Group Composite Scheme of Arrangement came into effect, transforming Gujarat Gas into an integrated energy company (renamed as Gujarat Energy), with the company now operating in the businesses of exploration & production of oil & gas, gas trading, gas transmission, power generation and city gas distribution. The gas transmission business has been demerged into GSPL Transmission, with the process for separate listing on BSE and NSE currently underway.

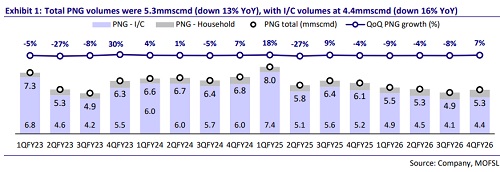

* Total city gas distribution volumes beat our estimate by 12% at 8.9mmscmd (down 5% YoY).

* While D-PNG volumes stood 7% below est., CNG volumes were 4% above our est. I&C-PNG volumes came in 26% above estimates at 4.4mmscmd.

* Gas trading volumes stood at 4.6/4.9mmscmd in 4QFY26/FY26.

* Standalone revenue stood at INR57.6b (-10% YoY, -3% QoQ).

* EBITDA stood at INR7.8b (+34% YoY, -18% QoQ). EBITDA margin came in at 13.6% (vs. 16.1%/9.2% in 3QFY26/4QFY25).

* APAT stood at INR5.7b (+15% YoY, -19% QoQ).

* In 4QFY26, the company incurred exceptional expenses of INR500m pertaining to stamp duty charges w.r.t. the amalgamation and made a provision of INR118m in respect of royalty & interest in the non-operated blocks where the company has a participating interest.

* The board has recommended a dividend of INR8.9/sh (FV: INR2/sh).

* The company added 7/14 new CNG stations in 4QFY26/FY26. It operates 839 CNG stations and supplies natural gas to over 2.4m households across six states and one union territory.

Valuation and view

* The company’s long-term volume growth prospects remain robust, with the addition of new industrial units and the expansion of existing units. It is aggressively investing in infrastructure to push industrial gas adoption in Thane rural, Ahmedabad rural, and newly acquired areas in Rajasthan.

* The stock (ex-GTL) currently trades at 13.5x FY28E P/E. We reiterate our BUY rating on the stock with an SoTP-based TP of INR490/sh. In our SoTP-based valuation, we value: 1) the city gas distribution segment at 12x FY28E EV/EBITDA (INR261/sh); 2) the gas trading segment at 5x FY28E EV/EBITDA (INR58/sh); 3) add FY28E net cash balance (INR86/sh); 4) the gas transmission business at 8x FY28E P/E (INR66/sh); and 5) investment in subsidiaries, associates, and JVs at 0.8x P/B (INR18/sh).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)