Buy Godrej Consumer Ltd For Target Rs. 1,450 by Motilal Oswal Financial Services Ltd

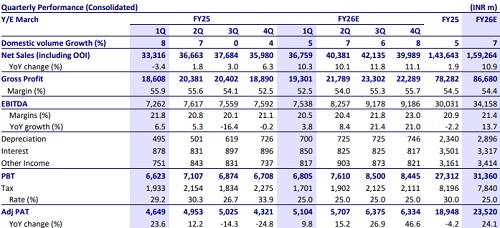

* Domestic demand continued to mirror 4Q trends, with rural outpacing urban demand. We model 8% standalone revenue growth and 5% volume growth. Price hikes likely persisted in 1Q, especially in soaps.

* High inflation continues to put pressure on margins. We model a 330bp YoY contraction in the GP margin and a 130bp YoY contraction in EBITDA margins. The benefit of lower palm oil prices will materialize from 2QFY26 onwards.

* The company highlighted in its pre-quarter update that the Personal Care segment is expected to deliver lowsingle digit value growth, impacted by soaps. The Home Care business is likely to deliver double-digit value growth and UVG.

* The Indonesia business expected to deliver flattish UVG while GAUM business is likely to deliver strong doubledigit value growth and UVG

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Retail Sector Update : QSR - QSR at an inflection point; risk-reward favorable By Motilal O...