Buy Fractal Analytics Ltd for Target Rs.980 by Choice Institutional Equities

Growing Enterprise AI Adoption to Create Structural Growth Opportunity

FRACTAL is a pure-play enterprise DAAI company delivering end-to-end consulting, implementation, and AI-led software solutions through an integrated model combining data science, design, behavioral science, and cloud engineering. FRACTAL addresses a ~USD 143 Bn DAAI services TAM as of FY25, expected to expand at 16.7% CAGR FY25-30E. The company is also a key player in the Global AI Software market, which is anticipated to witness 22.9% CAGR FY25-30E.

Product and Platform Strategy Expands Long-Term Monetization

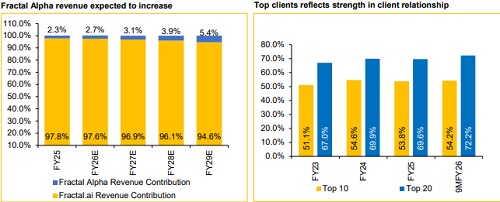

FRACTAL has built a differentiated AI-led IP ecosystem supported by a growing patent portfolio, anchored by Fractal.ai segment including platforms such as Cogentiq, MarshallGoldsmith.ai, Kalaido.ai, Vaidya.ai, and Trial Run. Additionally, through its incubation arm Fractal Alpha segment it is creating growth optionality by scaling highpotential ventures like Asper.ai and Analytics Vidhya. As of Jan 2026, FRACTAL holds a strong patent portfolio (66 filed, 24 granted), including 18 patents filed under Asper.ai, of which 6 have been granted. Disciplined M&A investment (INR 5,581/ USD 74 Mn in FY22–FY25) has accelerated Fractal’s shift to IP-led growth, scaling up high-margin AI platforms and strengthening talent moats.

Premium Enterprise Client Base Driving Strong Land-and-Expand Growth

FRACTAL focuses on Must Win Clients (MWCs) which contribute 83% to the revenues which have grown double-digit consistently on a higher base, (19% YoY growth in 9MFY26) supported by long-standing relationships with global blue-chip enterprises such as Citi Bank, Costco, Franklin Templeton, Mars, Mondelez, Philips, and Nestlé, and also served “Magnificent Seven” companies. High client stickiness is reflected in strong NRR (114%) and 8+ year average top-client tenure. FRACTAL is uniquely positioned at the enterprise AI application layer, leveraging models from OpenAI and Anthropic to deliver domain-specific solutions, supported by its pure-play AI focus and strong proprietary IP across the DAAI value chain. Unlike diversified IT services and product-centric peers, the company follows a hybrid model combining proprietary GenAI platforms with high-value services, enabling scalable, enterprise-grade AI deployments.

Valuation & View

FRACTAL’s strong positioning in DAAI Value chain provides significant growth headroom as enterprise AI adoption expands. Moreover, increase in high gross-margin (~70%+) subscription-led revenues (currently contributes ~3%) versus the company average gross margin of 46%, supports improved qualitative growth with further margin expansion. We expect Revenue/EBIT/PAT to grow at a CAGR of 22.8%/40.6%/46.2% over FY26E–FY29E. Factoring in strong structural long-term tailwinds driven by accelerating AI adoption, we initiate coverage with a BUY rating deriving a DCFbased target price of INR 980, implying a P/E multiple of 30x on FY28E EPS of INR 32.4 (22.3% upside from CMP). Stronger MWC growth led by growth in NRR and faster subscription adoption present upside potential, while slower execution poses downside risk.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131