Buy Elecon Engineering Company Ltd For Target Rs.635 by Axis Securities

Precision in Motion

We are initiating coverage on Elecon Engineering Company Ltd. (Elecon). Established in 1951 and headquartered in Gujarat, Elecon is a leading Indian manufacturer of industrial gear systems and material handling equipment. As Asia’s largest gear manufacturer, it caters to critical sectors including power, steel, cement, and mining. The company has built a strong global presence through subsidiaries in Europe and the U.S., strengthened further by the Benzlers–Radicon acquisition. With a longstanding reputation for engineering excellence and innovation, Elecon delivers comprehensive, end-to-end industrial solutions, positioning it as a key player in the capital goods and heavy engineering space.

Investment Thesis

* Proven manufacturing capabilities and diversified customer base: Elecon’s Gear Division is Asia’s largest industrial gear facility, manufacturing a broad range of customised gearboxes, including helical, bevel, planetary, worm, and marine gear systems. In the Material Handling Division, the company’s systems are deployed across India and international markets, serving power, mining, steel, cement, and port sectors. Strong backward integration provides Elecon with control over design, prototyping, and the broader supply chain, supporting consistency in quality and delivery across domestic and global operations. Its diversified and marquee customer base reduces dependence on any single sector or client, while nearly 70% of the company’s customers are repeat clients.

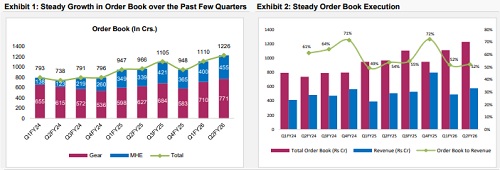

* Growing order book, robust domestic and global demand: The company’s combined order book stands at Rs 1,302 Cr as of 30 September 2025, marking a 20% YoY increase. This steady expansion in the order book over recent quarters indicates strong revenue visibility. Within India, increased spending across power, steel, sugar, marine, defence, and cement sectors that form Elecon’s core customer base is expected to further strengthen demand. The company also maintains a meaningful presence in key international markets, where improving industrial cycles are likely to drive additional demand for its product portfolio.

* Favorable government policies to accelerate domestic demand: Favourable government policies aimed at strengthening domestic manufacturing are expected to accelerate capital investments in India. Initiatives such as the PLI scheme and Make in India are set to support growth across Elecon’s core sectors. The MHE division, in particular, is closely linked to the broader capex cycle and is therefore positioned to benefit meaningfully from any pick-up in private sector capex.

* Focus on exports to aid revenue growth and profitability: Elecon maintains a broad global footprint across Asia, the Middle East, the USA, the UK, Europe, and Africa. Although geopolitical disruptions affected select markets in recent quarters, demand prospects remain firm, supported by healthy inquiry pipelines across most international regions. The company is intensifying efforts to strengthen its global presence through targeted brand-building initiatives and by establishing rapid build centres, complementing its existing operations in the U.S. and Europe. As newly expanded capacity ramps up and international contributions rise, the company is positioned to achieve further margin improvement over the medium term.

Valuation & Recommendation

We initiate coverage on Elecon Engineering Ltd. with a BUY recommendation. For FY26, the company has maintained a revenue guidance of Rs 2,650 Cr and EBITDA margins above 24% This implies an impressive revenue growth of 20% YoY in H2FY26 over H2FY25. Moreover, in H2FY26, the company is expected to deliver a notable 48% revenue growth over H1FY26. Over the medium term, the company is expected to sustain this momentum. This will be driven by a) Order book growth of 19% (CAGR) over FY25-28E, supported by robust demand from key end markets, b) Timely capacity expansions coupled with stronger R&D capability and export focus, c) Improved profitability with EBITDA margins reaching above 25%, and d) Enhanced free cash flows (~2x in FY28E vs FY25). Accordingly, we expect Revenue/EBITDA/PAT to grow at 19%/21%/17% CAGR over the FY25-FY28E period. The stock currently trades at a Sep’27E PE of 19x, and we value the stock at 24x of Sep’27E EPS, translating into a target price of Rs 635/share. This implies an upside of 27% from the CMP.

For More Axis Securities Disclaimer https://simplehai.axisdirect.in/disclaimer-home

SEBI Registration number is INZ000161633