Buy CreditAccess Grameen Ltd for the Target Rs.1,600 by Motilal Oswal Financial Services Ltd

From repair to re-acceleration: RoE recovery in motion

Margin improvement and credit cost normalization to drive earnings rebound

* CreditAccess Grameen (CREDAG) is emerging from the recent MFI stress phase with improving operating momentum, resilient portfolio retention, and a structurally stronger business mix. The normalization of asset quality trends, combined with retail finance-led diversification and improving spreads, positions the company for a sharp earnings recovery in FY27–28E.

* Despite accelerated write-offs during the stress cycle, CREDAG has broadly retained its AUM — a relative outperformance versus peers that witnessed sharper portfolio contraction. This resilience reflects strong borrower stickiness, with ~70–80% of disbursements extended to existing customers, and a meaningful normalization in group repayment behavior.

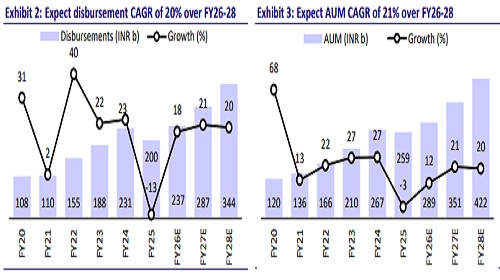

* Retail finance is now emerging as the key structural growth engine. Its share in AUM has risen from ~11% to ~14% in Dec’25 and is likely to drive overall AUM growth at 20%+, even as MFI (JLG) growth moderates to low teens (~10–12%). Over the medium term, management aims to achieve a balanced secured– unsecured mix within retail finance, strengthening portfolio diversification. ? With Karnataka stress largely normalized and PAR accretion moderating sharply, credit costs are set to decline meaningfully. Excluding the Karnataka ordinance impact, FY26 credit cost would have been ~3.5–4%, highlighting the underlying strength of the franchise.

* We model an AUM/NII/PPoP/PAT CAGR of 21%/16%/13%/50% over FY26–28E, with RoA/RoE improving to ~4.5%/~17.5% by FY28E. At ~2.3x FY27E P/BV, the stock remains attractively valued. We reiterate our BUY rating with a TP of INR1,600 (premised on 2.4x Dec’27E BVPS).

From stabilization to scale: gears up for 20%+ AUM growth

* CREDAG added ~165 branches in 9MFY26, taking its footprint to ~2,222 branches. The company continues to follow a district-wise saturation model, limiting concentration risk with no district contributing more than ~3–4% of GLP.

* Borrower acquisition remained steady, with ~640k additions during 9MFY26 despite MFIN guardrails. Importantly, ~50% of incremental borrowers were sourced outside the top three states, reflecting improving geographic diversification.

* A key positive development has been the normalization of group dynamics. Earlier instances of delinquent borrowers influencing collective nonpayment have materially reduced, leading to healthier repayment patterns. PAR 15+ accretion declined sharply from 0.84% (in Mar’25) to 0.18% (in Dec’25), reflecting improving portfolio behavior.

* Despite elevated write-offs, AUM has been broadly retained. This underscores disciplined underwriting and superior field execution.

Retail finance: Structural diversification and the next leg of growth

* Retail finance continues to outpace MFI growth, supported by the graduation of vintage borrowers into individual lending products. The unsecured individual portfolio comprises 1) Unnati loans (~INR200k ATS and AUM of ~INR17b) for evolved borrowers and 2) Vishesh loans (~INR80k ATS and AUM of ~INR16b) for emerging customers.

* Asset quality across both segments remains strong, with PAR 30+ below ~2%. Importantly, unsecured loans are extended only to graduated ecosystem borrowers with no open-market sourcing, which significantly reduces underwriting risk.

* Mortgage products follow a balanced sourcing approach (~50% internal/ ~50% open market); CREDAG intends to accelerate scaling in this segment.

* Over the medium term, CREDAG aims to move toward a ~50:50 secured– unsecured mix within retail finance. While MFI growth is expected at ~10–12%, retail finance is likely to grow above 20%, supporting the overall AUM CAGR of ~21% over FY26E-28E.

Spreads to expand; reducing interest income reversal to support NIM

* CREDAG expects portfolio yields to rise toward ~21.5%, implying ~30-50bp improvement from current levels. Borrowing costs are expected to stabilize at ~9.2-9.3%, with limited further reduction. This could translate into a spread expansion of ~50-60bp.

* About 65% of the borrowings are linked to short-tenor MCLR rates (3-9 months), enabling quicker transmission of lower funding costs. Additionally, lower interest reversals as asset quality stabilizes should support NIM. We model NIM (calc.) at ~14.9% in FY27–28E.

Operating leverage to play out over the next two years

* CREDAG’s business support framework flexibly adapts to operating conditions – pivoting between process efficiency during stable periods and PAR management during stress cycles.

* Management has not materially altered its cost structure nor added significant collection manpower, indicating confidence in existing systems. While absolute opex may rise with expansion, positive operating leverage is expected to emerge as branch productivity improves.

* We expect the C/I ratio to remain in the 33–34% range over FY26–28E, with gradual improvement in opex-to-assets.

Asset quality stabilizing; credit costs normalizing

* Karnataka stress has largely normalized, while UP, Bihar, and MP continue to show gradual YoY improvement. January PAR accretion has moderated, though sustained improvement remains key.

* CREDAG’s underwriting remains disciplined, driven by 1) system-driven MFI lending, 2) detailed cash flow and field assessments for individual loans, and 3) a weekly repayment structure (for ~65% of the borrowers) enabling early stress detection.

* Management guides credit cost at ~3–3.5% (aspiring toward ~2.5-3.0% as normalization strengthens). We model credit costs of ~6.6% in FY26, declining sharply to ~3.5%/~3.4% in FY27/FY28E.

Valuation and view

* CREDAG is transitioning from a stress-recovery phase to a structurally stronger growth trajectory, supported by retail-led diversification, margin resilience, and embedded risk discipline.

* We model an AUM/NII/PPoP/PAT of 21%/16%/13%/50% over FY26-28E with an RoA/ RoE of ~4.5%/17.5% by FY28E.

* At ~2.3x FY27E P/BV and ~14x FY27E P/E, CREDAG’s valuations remain reasonable relative to the medium-term RoE potential of ~17-18%. As credit costs normalize and earnings visibility brightens, we see scope for gradual rerating. We reiterate our BUY rating with a TP of INR1,600 (premised on 2.4x Dec’27E BVPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412