Buy Colgate Palmolive (India) Ltd For Target Rs. 2,850 by Motilal Oswal Financial Services Ltd

Ltd ( 1 ).jpg)

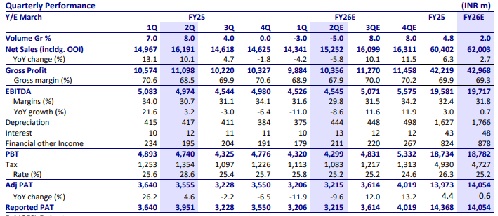

* Demand was subdued for oral care. We expect 6% revenue decline, led by 5% volume decline in toothpaste in 2Q.

* Moreover, channel destocking due to revised GST rates (from 18% to 5%) impacted 2Q performance.

* GP margin is expected to contract 60bp YoY to 67.9%, while EBITDA margin is expected to contract 90bp YoY to 29.8%, given higher ad spends and operating activities.

* The company is focused on expanding distribution reach and improving product penetration in the rural market through LUPs.

* Promotions in the GT channel and the quantum of discounting in alternate channels will be the key monitorables.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Financials Banking Sector Update : Reconciling banking business updates with systemic data b...