Neutral Colgate Ltd for the Target Rs 2,500 by Motilal Oswal Financial Services Ltd

Ltd ( 1 ).jpg)

Beat on revenue; positive outlook for FY27

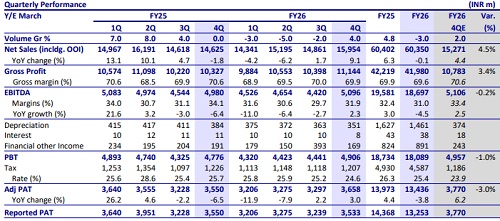

* Colgate (CLGT) delivered 9% YoY revenue growth to INR16.0b (est. INR15.3b, two-year CAGR 3%) in 4QFY26. Volume growth stood at 4% (est. 2%), clocking growth after three consecutive quarters of decline. The company reported flat revenue and a volume decline of 1.5% in FY26.

* Urban demand improved sequentially during the quarter, while rural growth moderated after outperforming over the past year. Management expects the gap between rural and urban growth to narrow going forward. Dabur’s oral care delivered mid-single-digit growth, and HUVR oral care delivered low single-digit revenue growth in 4Q.

* Gross margin contracted 80bp YoY to 69.9% (est. 70.6%). Management indicated low single-digit pricing actions ahead to offset inflationary pressures. EBITDA margin contracted 210bp YoY to 31.9% (est. 33.4%, 31% in FY26), impacted by higher ad spends (+10% YoY) and GST-related inverted duty structure (~160bp impact in 4QFY26, 80bp in FY26).

* Heading into FY27, management reiterated its focus on driving balanced growth through volume recovery and selective pricing actions, while continuing to invest in brands and premiumization initiatives to support top-line growth. We model an 8% revenue CAGR and 11% EBITDA CAGR over FY26-28E. We reiterate our BUY rating on the stock with a TP of INR2,500 (based on 40x Mar’27E EPS).

Key highlights from management commentary

* Premium portfolio contribution increased 35% over the last two years, led by stepped-up investments in Colgate Total, Visible White, and Periogard.

* Gross margins should remain broadly stable over the next two quarters despite commodity and currency inflation. Management highlighted that the EBITDA trajectory will depend on incremental advertising investments rather than margin maximization.

* E-commerce now contributes ~10% of the overall business.

* Direct reach expanded to 1.7m outlets with the addition of ~200k stores during FY26.

Valuation and view

* There are no material changes in our EPS estimates for FY27 and FY28.

* Heading into FY27, management reiterated its focus on driving balanced growth through volume recovery and selective pricing actions, while continuing to invest in brands and premiumization initiatives to support top-line growth. We model an 8% revenue CAGR and 11% EBITDA CAGR over FY26-28E. We reiterate our BUY rating on the stock with a TP of INR2,500 (based on 40x Mar’27E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Ltd.jpg)