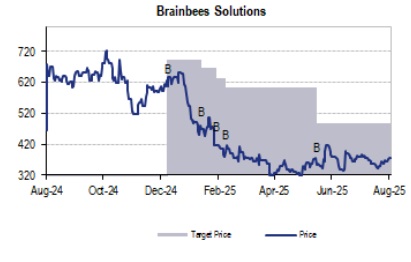

Buy Brainbees Solutions Ltd for the Target Rs. 460 by JM Financial Services Ltd

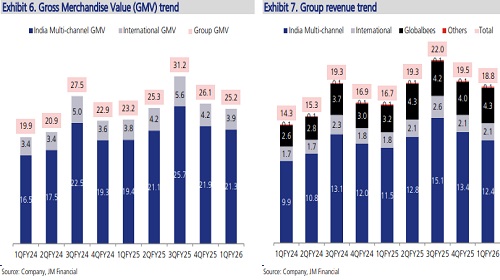

FirstCry reported a muted 1QFY26, with IMC GMV growth moderating to 9.7% YoY due to slower offline growth and operational disruptions, whereas International GMV grew only 3.3% YoY. GlobalBees remained a key growth driver with 31.4% YoY revenue growth led by core brands. Consolidated gross margin expanded 80bps YoY to 38.5% due to increased mix of home brands; however, adj. EBITDA margin inched up only 50bps YoY to 5.0% due to higher fulfilment costs driven by last-mile delivery investments. While quarter’s performance was impacted by weaker offline performance amid discretionary slowdown, strong brand positioning, rising home brand salience, and omni-channel presence, coupled with store expansion plans, position the company for a healthier growth and margin expansion ahead. We maintain ‘BUY’ rating with revised SoTP-based Jun’26 TP of INR 460.

* India Multi-channel (IMC) impacted by lower offline growth: IMC segment saw GMV growth of 9.7% YoY, a miss on JMFe by 3%. Growth was driven by 14% YoY growth in transacting users, though order volume grew 6% only. The moderation in growth was mainly due to 1) challenges in last-mile delivery leading to bad customer experience, 2) slowdown in offline business due to muted demand environment, untimely rainfall and closure of 38 COCO stores in 3Q, and 3) operational disruptions due to geopolitical tensions. Revenue stood at INR 12.4bn, 7.5% YoY growth. We believe that moats for FirstCry remain intact with BabyHug being the largest childcare brand in the country and private labels accounting for c.55% of the GMV in FY25. Gross margin expanded 120bps YoY due to increasing home brands salience; however, Adj. EBITDAM saw a rise of just 30bps YoY to reach 8.6%. Management aims for early-teens revenue growth in FY26 as demand is improving in July’25. Company plans to add ~90-100 COCO stores in FY26.

* GlobalBees delivers robust growth led by ‘Core’ brands: GlobalBees experienced strong revenue growth of 31% YoY to reach INR 4.3bn. Management has been deliberately reducing ‘Other brands’ to focus on ‘Core categories’, which have grown significantly faster at 40% YoY. However, rationalisation of ‘Other brands’ led to margin contraction with Adj. EBITDAM declining 40bps YoY to reach INR 41mn. Adj. EBITDA from core brands has been at ~4.5% (post corporate expenses). Others segment, which primarily includes Education, delivered INR 131mn in revenue, 9.4% YoY (+20.5% QoQ) growth.

* Margin and profitability: In 1QFY26, gross margin (GM) improved to 38.5%, 80bps YoY (+100bps QoQ) improvement. Growth was supported by an increase in home brands in overall mix, increase in share of Kids & Babies Fashion in GMV and rising home brand and third party margins due to economies of scale. However, Adj. EBITDA margin improved only 50bps YoY (-20bps QoQ) to 5.0%. As a result, Adj. EBITDA stood at ~INR 0.93bn in 1Q (24.8% YoY/-7.7% QoQ). Margin improvement was lower than GM expansion due to 1) increased fulfilment cost 2) investments done to improve last-mile delivery 3) revenue mix has shifted towards GlobalBees, which is a lower margin business vs. IMC business. Management noted that India Multi-channel is yet to reach its steady-state EBITDA margin, and margin expansion will continue over the next 4-5 years.

* Maintain ‘BUY’ with reduced Jun’26 TP of INR 460 (vs. INR 478 earlier): We lower revenue estimates marginally (1-5% over FY26-29E) considering drag from International business and muted performance in IMC business since past few quarters. Estimate cut are not sharper because we believe IMC business to benefit from recovery of demand environment. We believe that losses in International segment have peaked now and hence should experience sharper margin recovery and hence we increase Adj, EBITDAM estimates for this business by 100-250bps over FY26-29E. However, IMC margins might see slower expansion and hence overall Adj. EBITDAM estimates cut is only 3-10bps. PAT estimates are increased by c.36% in FY26 due to higher than expected other income. We expect the company to deliver c.13% revenue growth over FY25-30, while Adj. EBITDA CAGR would be ~38%, driven by sustained margin expansion across segments. We continue to value India Multichannel / GlobalBees Brands / Others at 35x / 30x /20x FY27E Pre Ind AS Adj. EBITDA while International segment multiple at 1.5x FY27E sales, resulting in reduced Jun’26 TP of INR 460. We recommend ‘BUY’.

* India Multi-Channel remains significantly undervalued for a 20%+ compounding play: While last few quarters have been undoubtedly a tough for FirstCry, its IMC segment still managed to deliver Adj. EBITDA growth of 24% in FY25. With growth recovery likely in FY26 onwards, we expect the segment to deliver 3-year EBITDA CAGR of c.22%. As shown in exhibit 1, at CMP, IMC only implies 31.3x Pre Ind AS Adj. EBITDA multiple, significantly lower than traditional retailers with lower growth and minimal margin expansion potential. Hence, the slightest hint of growth recovery could be a significant rerating event for FirstCry.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361

.jpg)