Buy Ashoka Buildcon Ltd For Target Rs. 230 By JM Financial Services

Weak execution, likely to improve in 2H26

Ashoka Buildcon’s (ABL) 2Q26 PAT at INR 428mn (down 13% YoY) was above JMFe of INR 344mn (consensus: INR 427mn) due to higher other income and lower interest costs. Execution was weak in 1H26 (down 22% YoY), impacted due to extended monsoon and delay in start of newly won projects. With weaker 1H26, ABL has lowered revenue growth guidance to flat YoY (earlier: 10% growth) which in also optimistic in our view and we have factored 8% decline. ABL remains confident of ramping up execution in 2H26. Gross debt remained flat QoQ at INR 23bn as on Sept-25. ABL completed monetization of 5 HAM assets and received INR 10.5bn with remainder of INR 1bn to come in 3Q26E. ABL targets to complete monetization of 5 BOT assets in Nov-25. Proceeds from above monetization will help deleverage the balance sheet. Given the muted execution in 1H26, we have cut EPS by 9%/3%/6% for FY26/27/28E. Valuations remain attractive at 10x/8x FY27/28 core EPS (adjusted for assets). Maintain BUY with revised SOTP based price target of INR 230.

* 2Q26 PAT beats JMFe led by higher other income/lower interest costs: ABL’s revenue declined 11% YoY to INR 12.7bn (JMFe: INR 13.3bn) impacted by extended monsoons and slow ramp-up of newly awarded projects. EBITDA grew by 4% YoY to INR 1.23bn (in-line) with margins improving by 130bps YoY/40bps QoQ to 9.7% (JMFe: 9.3%). Interest cost grew by 11% YoY to INR 782mn but was below JMFe of INR 830mn. Other income declined by 12% YoY to INR 365mn but was above JMFe of INR 300mn. Adjusted PAT at INR 428mn was above JMFe of INR 344mn (consensus: INR 427mn) due to higher other income and lower interest costs. Reported PAT at INR 1.4bn included gain of INR 964mn (post-tax) on sale of 1 HAM asset.

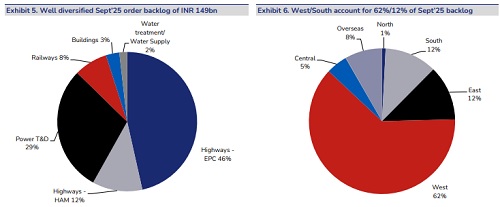

* Execution to improve in 2H26; cuts revenue guidance: With muted order inflows of INR 31bn in 1H26, ABL’s order backlog moderated to INR 149bn (2.3x TTM revenues) as of Sept-25. Supported by a healthy bid pipeline across segments, ABL is expecting order inflows of INR 100bn for FY26E. Given the weak execution trend in 1H26 (down 22% YoY) and delay in rampup of new projects, ABL has lowered its FY26E revenue growth guidance to flat YoY (earlier: 10% growth), with EBITDA margins of 10%. We believe even flattish revenue guidance is optimistic and have factored 8% decline in FY26E. Execution is expected to pick up gradually from 2H26 onwards.

* Asset monetization to help pare debt: ABL targets to complete monetization of 5 BOT assets in Nov-25 with gross inflow of INR 23bn, of which INR 17.5bn expected to be received in Nov25 and the balance by FY28. Monetization of 5 HAM assets was completed in 2Q26 of which INR 10.5bn has been received and remainder INR 1bn is expected in 3Q26. Further, sale of 6 HAM assets is expected to be completed by Jun-26 with inflows of c.INR 11bn. Additionally, ABL expects to monetize Chennai ORR by Mar-26 and Jaora by FY27. Post payment of c.INR 15.3bn to SBI-M, remainder proceeds will be used to pare debt.

* Maintain BUY with SoTP based revised price target of INR 230: Given the muted execution in 1H26, we have cut EPS by 9%/3%/6% for FY26/27/28E. Having said that, we expect robust core EPS CAGR of 45% over FY25-28E mainly led by revenue growth and margin expansion in FY27/28E. Currently, ABL trades at attractive valuations of 10x/8x FY27/28E core EPS (ex-other income) after adjusting for value of assets. Current valuations are at discount to peers but have room to re-rate if asset monetization goes as planned leading to balance sheet deleveraging. We value ABL’s EPC business at 12x Sept-27E core EPS, assets at INR 52 on P/B basis to arrive at an SOTP-based revised price target of INR 230. Maintain Buy.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361