2025-10-15 05:04:45 pm | Source: Motilal Oswal Financial Services Ltd

Buy Ashok Leyland Ltd for the Target Rs. 166 by Motilal Oswal Financial Services Ltd

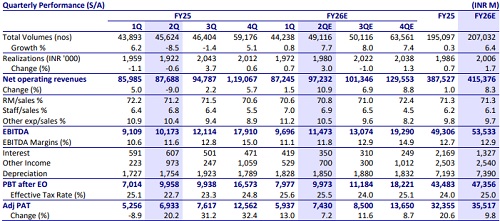

* After a subdued 1Q, CV volumes saw a healthy pickup in 2Q, up 7.7% YoY. While MHCV sales grew 9%, LCV sales rose 5.5%. Export mix has sharply improved, up 45% YoY.

* Input cost to largely remain stable QoQ, unlike fears of an increase. Staff cost may rise QoQ due to annual increments.

* Led by improved mix and volumes, EBITDA margin to rise 70bp QoQ (+20bp YoY) to 11.8%. PAT to grow 7% YoY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Disclaimer:

The content of this article is for informational purposes only and should not be considered financial or

investment advice. Investments in financial markets are subject to market risks, and past performance is

not indicative of future results. Readers are strongly advised to consult a licensed financial expert or

advisor for tailored advice before making any investment decisions. The data and information presented

in this article may not be accurate, comprehensive, or up-to-date. Readers should not rely solely on the

content of this article for any current or future financial references.

To Read Complete Disclaimer Click Here

Latest News

Quote on Markets by Mr Avinash Agarwal, Senior Vice ...

Uttar Pradesh continues to play a pivotal role in th...

Research report on Manthan- Oil & gas by Swarnendu B...

Market Round-up - 11th August 2026 by Motilal Oswal ...

India's Q1 FY27 GDP growth likely to near 8 pc amid ...

Buy Dalmia Bharat Ltd For Target Rs. 2,278 By Geojit...

Evening Roundup : Daily Evening Report on Bullion, B...

NASA invites ISRO to join Moon Base Programme as Ind...

Buy Suzlon Energy Ltd For Target Rs.56 By Geojit Fin...

India's merchandise exports touched record high at $...

More News

Retail Sector Update : QSR - QSR at an inflection point; risk-reward favorable By Motilal O...

Automobiles Sector Update : Retail demand trends seem encouraging across segments by Motilal Oswal Financial Services Ltd

Textiles Sector Update : Strong 1H growth expected; major capex announcement awaited by Motilal Oswal Financial Services Ltd

Automobiles Sector Update : MSIL/TMPV outperform in PVs, TVS in 2Ws, and TMCV in CVs by Motilal Oswal Financial Services Ltd