Buy Aditya Birla Real Estate Ltd for the Target Rs. 1,750 by Emkay Global Financial Services Ltd

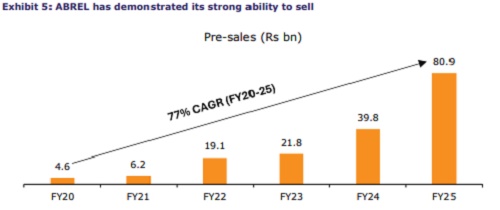

We reinitiate coverage on Aditya Birla Real Estate (ABREL) with BUY and TP of Rs1,750, based on 6x EV/embedded EBITDA, at a 27% premium to the NAV (currently, the stock is trading at 6% discount to the NAV). ABREL has demonstrated its ability to sell with cumulative sales booking of ~Rs178bn since the launch of its first residential project in Kalyan in 1QFY20. Pre-sales grew from Rs4.6bn in FY20 to Rs80.9bn in FY25 – a robust CAGR of 77%, with 78% of current projects already sold out. ABREL posted pre-sales of Rs38.5bn in 9MFY26. On the back of strong launches (GDV of Rs62bn) and healthy demand in 4QFY26, we expect the company’s FY26E pre-sales to cross the Rs84bn mark (vs Rs80.9bn in FY25). However, business development has been muted, with only one deal (GDV of Rs17bn) announced compared with GDV guidance of Rs150bn in FY26. We expect business development to pick up going forward, with several large projects across markets in the pipeline; FY26E/27E/28E pre-sales is projected at Rs84bn/84bn/118bn, respectively. Key monitorables are business development and launch of Niyaara

Ambitious growth plan

Although ABREL started its real estate journey in FY20 with pre-sales of Rs4.6bn, FY22 marked the launch of its first major project—Niyaara, in Worli. In FY22, it posted pre-sales of Rs19.1bn (mainly contributed by Niyaara). Since then, ABREL has continued to report strong pre-sales growth, and we expect FY26E pre-sales to more than quadruple to Rs84.0bn, implying a CAGR of 45% over FY19-26E. The company has set a strong ambitious pre-sales target of Rs150bn by FY28, at 34% CAGR over FY26-28.

Capital backing in place for the ambitious growth plan

Two project-level private equity deals in FY26 helped generate funds for ABREL, amid the high debt overhang. Also, sale of the paper business (~Rs34.98bn) to ITC is likely to be concluded shortly, with proceeds expected to be received soon. The company’s target of achieving Rs150bn annual pre-sales by FY28 is well-supported by this capital framework and the existing (at end-9MFY26) cash flow visibility of Rs70.0bn from ongoing projects.

Presence in all the top-four markets – NCR, MMR, Pune, and Bengaluru

Within a short span of its foray into the real estate business, ABREL has expanded its footprint across India’s top-four markets, with cumulative pre-sales contribution of 38% from MMR, 33% from NCR, 25% from Bengaluru, and 3% from Pune. Strong launch responses across markets are also a testament to its ability to sell across regions.

Valuation – Trading at a discount to the NAV

We assume pre-sales of Rs118bn in FY28E, a conservative EBITDA margin of 25%, and a 6x embedded EBITDA multiple. The company currently trades at 6% discount to the NAV, despite a consistent strong pre-sales performance and 25-30% embedded EBITDA. Given ABREL’s strong cashflow visibility, ability to sell, and impeccable corporate governance, we believe the stock is likely to trade at a significant premium to the NAV.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354