Add Wipro Ltd for Target Rs.285 by Choice Institutional Equities

.jpg)

Directionally Positive; Recovery remains delayed

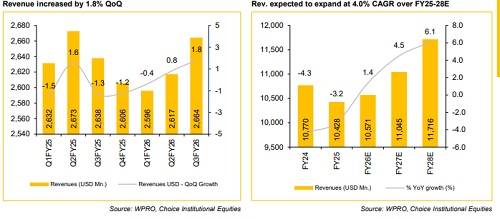

View and Valuation: WPRO delivered a resilient Q3FY26 performance, driven by the ramp-up of the Phoenix deal and inorganic revenues from Harman DTS. However, delays in ramp-ups of two mega deals in the Healthcare and BFSI verticals are likely to limit their contribution to Q4 revenues, which will also be impacted by lower working days. While momentum in AI and engineering remains strong, deal conversions are expected to be gradual. Thus, we expect Revenue/EBIT/PAT to grow at a CAGR of 6.9%/6.0%/6.7% over FY25–FY28E and maintain our ADD rating with a target price of INR 285, based on FY27E & FY28E average EPS of INR 14.3 at a P/E multiple of 20x.

Margin Expansion Supported by Modest Revenue Growth

* WPRO reported Q3FY26 IT services revenues at USD 2,635 Mn, up 1.2% QoQ, while in CC terms growth stood at 1.4% QoQ (Harman DTS acquisition contributed 0.8% to CC growth). Total revenues including Product revenues, were up 1.8% QoQ in USD terms, while in INR terms total revenue stood at INR 235.6 Bn, up 3.8% QoQ.

* Operating (EBIT) Margin for IT Services came at 17.6% for Q3FY26, up 90 bps QoQ. However, overall EBIT margin remained almost flat at 16.1% QoQ led by lower margin of Product segment.

* PAT for the quarter came in at INR 31.2 Bn, down 3.9% QoQ including impact of Labour code one-off expenses of INR 3028 Mn. EPS for Q2FY26 stood at INR 2.9.

Resilient growth despite Seasonality, supported by inorganic contribution from Harman DTS: WPRO’s Q3FY26 total contract value stood at USD 3.3 Bn, down 28.9% QoQ, with large-deal TCV at USD 0.9 Bn, down 69% QoQ. Deal wins were primarily led by cost optimisation, vendor consolidation, and AI-led transformation initiatives, with the company increasingly building consulting-led AI solutions across verticals. Amongst verticals, Technology & Communications grew 4.2% QoQ, supported partly by the Harman DTS integration, while Healthcare also grew 4.2% QoQ aided by seasonal and platform-led demand. BFSI remained resilient with 2.6% QoQ growth, although Capco was impacted by furloughs despite a steady pipeline. Consumer and Manufacturing continued to face pressure due to tariff-related uncertainty, though pipeline visibility is improving, particularly in Europe and the Americas. Overall, Wipro’s strategic positioning around AI and engineering services provides downside protection, reinforcing a stable outlook supported by large deal momentum.

WPRO intends to hold Margin, despite Integration and Investments:

WPRO reported EBIT margin of 17.6% in IT Services, the highest level in several quarters, reflecting strong operational discipline. Management reiterated its intent to sustain margins in the 17–17.5% range, while factoring in incremental dilution from the HARMAN integration, ongoing investments and planned wage hikes. Continued investments in AI, talent upskilling and transformation capabilities are strategically important for long-term positioning, though they may constrain nearterm margin expansion. The company emphasized a balanced approach of protecting profitability while selectively investing for growth. Delayed deal rampups during the quarter mitigated seasonal headwinds, while gradual ramp-ups ahead are expected to aid revenue growth and margin improvement.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

2.jpg)