Accumulate Elgi Equipments Ltd for the Target Rs.603 by PL Capital

Domestic strength and export market share gains

Quick Pointers:

* Company guides for revenue of Rs38.8bn with an EBITDA margin of ~14.6% in FY26.

* Elgi’s strategic business plan envisages ~11% revenue growth CAGR over FY26-31E driven by India (~12% CAGR) and RoW (~10% CAGR).

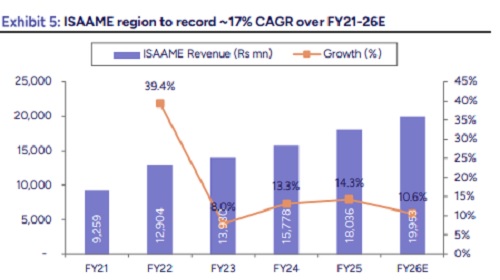

We attended Elgi Equipments’ (ELEQ) analyst meet, where management highlighted business performance, product innovation, and its medium-term strategic roadmap. The ISAAME region is expected to remain the key growth engine, supported by strong traction in the Middle East and a recovery in investment activity following tariff normalization. In North America, performance was weighed down by the structurally lower-margin portable segment and prior tariff impacts; however, underlying initiatives remain intact. Europe has achieved break-even following cost rationalization, with future growth anchored in market share gains across core markets. In Australia, share gains have partially mitigated broader market weakness. Rising traction for Demand=Match and a robust pipeline of new product launches position the company well to achieve its USD750mn revenue target with ~18% EBITDA margin by FY31, reinforcing a constructive long-term outlook. The stock is currently trading at a PE of 36.0x/31.4x on FY27/28E earnings. We roll forward to Mar’28E and maintain our ‘Accumulate’ rating valuing the stock at a PE of 35x Mar’28E (35x Sep’27E) arriving at a revised TP of Rs603 (Rs565 earlier).

Despite the recent macro-economic boost via tariff reduction and India-EU FTA, the pace of the recovery of the European market will be key monitorable in short to medium term. Meanwhile, we believe ELEQ is poised for healthy long-term growth on the back of 1) it being among top 2/10 players in the Indian/global air compressors market, 2) technology development along with strong backward integration, 3) its growing global installed base driving high margin aftermarket sales, 4) new product launches, and 5) market leadership in automotive garage equipment.

The next leg of growth; envisaged ~11% growth CAGR over FY26-31E: The company has outlined a five-year Strategic Business Plan (FY26-FY31), targeting revenue of USD750mn (~Rs66.2bn), implying an ~11% CAGR over the period. Growth is expected to be predominantly India-led (~12% CAGR), while the Rest of the World is projected to grow at ~10%. In India, momentum will be driven by market share gains, new product introductions, increased penetration of existing offerings, and geographic expansion, while exports are likely to benefit from aftermarket growth in Europe supported by a rising installed base. Product-wise, Accessories (dryers), Aftermarket, and oil-lubricated screw compressors are expected to anchor the next phase of growth.

Above views are of the author and not of the website kindly read disclaimer