Diet Report - Eternal Platform fee hike adds margin tailwind by Elara Capital

Eternal ( ZOMATO IN) has raised its platform fee by ~20% to ~INR 15/order, aligning it with Swiggy ’s level . We estimate each INR 1 hike drives ~26bp take -rate expansion and ~INR 1.2bn incremental adj EBITDA (~5% of base). In our base case (50% market implementation at INR 15), th is add s ~40bp to the take rate and ~INR 1.8bn (~7.5%) to FY27E adj EBITDA . At 3.1% of food delivery ( FD ) Average order value (AOV ) of ~INR 475, the fee remains too low to trigger demand elasticity, supported by Monthly transacting users (MTU ) growth accelerating to ~22% in Q3FY26. The move supports management's 5 – 6% adj EBITDA/GOV target ; we expect 6% by FY28E . The fee hike largely factored in our base case Adj. EBITDA margin estimates for FY27E; thus , we keep our estimates unchanged. We retain Buy with a TP of INR 415 per share as we value food delivery on 55x EV/EBITDA, Blinkit on 5x EV/gross profit and Going out / Hyper pure on 3x EV/Sales .

Zomato to benefit from the platform fee hike: Zomato has increased its platform fees by ~ 20% to INR 15 per order. With this, its platform fee is at par with Swiggy ’s INR 15 per order. As per our estimates, every INR 1 increase in platform fee should result in Zomato see ing a ~26bp positive impact on the take rate and an incremental adj EBITDA impact of ~INR 1.2bn (~ 5% of adj EBITDA) . A s a base case where fee hike implementation in 50% of markets, incremental INR platform fee should drive 40bp gain in the take rate, a 7.5% uplift in FY27E adjusted EBITDA of INR 1.8bn . The current hike is directi onally in line with guidance of achieving adj EBITDA in the band of 5 -6%, thereby factor ing in the fee hike. As on Q3FY26, Zomato ’s adj EBITDA was at 5.4%, and estimated to reach 6.0 % by FY28E.

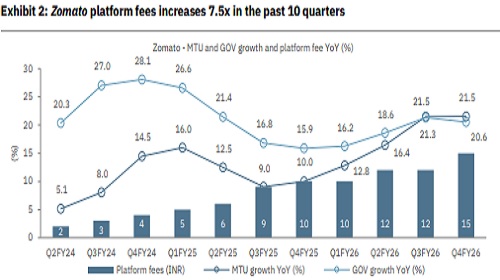

GOV growth remains robust: Platform fees have increased 7.5x since their introduction in August 2023 (INR 2 initially) ; sinc e th en , Zomato has hiked them in almost every quarter. company data shows a g radual increase in platform fees has not affected the gross order value (GOV ) growth rate, although the overall food industry slowdown dragged GOV growth during Q3FY25 -Q2FY26 ; FD GOV growth rebounded to 20%+ in Q3FY26. The growth comeback is led by MTU, which saw growth acceleration from 9% in Q3FY22 to ~22% in Q3FY26. Better user growth momentum should aid in elasticity and Zomato ’s ability to charge higher platform fees .

Higher fee would not trigger elasticity: Increased fee of INR 15 per order is currently at 3.1% of FD AOV -- INR 475 as per our estimate , which is not adequate to trigger any meaningful elasticity for consumers. Moreover, the platform fee is in line with its peer, Swiggy . Hen ce, Zomato’ s increased platform fee should not pose concern over order flows. Platform fee has been one o f the trigger s for adj EBITDA margin ; guidance of 5 -6% of adj net order value (NOV ) band i nclude s such platform fee hikes ; We model a ~40bps increase in Adj. EBIDA in FY27E, which broadly factors 50% implementation of increased fees, however, a pan India implementation shall drive upgrade . With the recent rebound in MTU growth, FD GOV growth momentum is set to sustain. We estimate a 6% adj EBITDA margin by FY28E . Further, we believe platform fee hike could also provide a cushion to EBITDA margins in the event of a rise in fuel prices. EV penetration within gig workers remains low, at ~10% in food delivery and ~20 -25% in quick commerce. In such a scenario, companies may have to compensate gig workers for higher fuel costs. As per our assessment, every 10% increase in fuel prices could have a negative impact o f nearly INR 0.9bn (INR 1 per order, assuming 20-25% is fuel cost and balance is Labour) on the food delivery EBITDA. Hence, the higher platform fee shall act as a partial hedge against such cost pressures going ahead. We retain Buy on ETERNAL with a TP of INR 415 per share.

Please refer disclaimer at Report

SEBI Registration number is INH000000933

More News

Defence & Aerospace Sector Update : Revenue softness due to execution timing, but margin & e...