Buy Eternal Ltd For Target Rs. 340 Motilal Oswal Financial services Ltd

Stable quarter, assured guidance

Long-term ramp intact despite near-term volatility

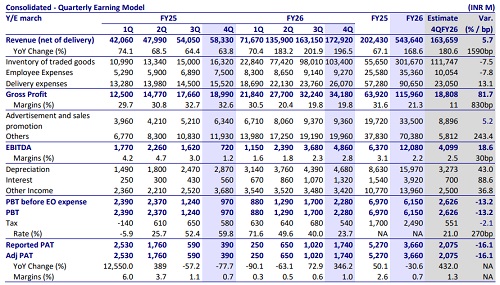

* Eternal reported 4QFY26 net revenue of INR172b, up 6% QoQ/196% YoY, above our estimate of 0.3% QoQ/181% YoY growth.

* Food delivery (FD) NOV came in at INR97.6b, above our est. of INR96.4b. Blinkit NOV came in at INR143.8b (up 96% YoY) vs. our est. of INR146b. For FD, adjusted EBITDA as a % of NOV margin was up 10bp QoQ at 5.5% vs. our estimate of 6.1%.

* Blinkit reported a contribution margin of 5.4% (5.5% in 2Q). Adj. EBITDA margin was at 0.3%, above our expectation of -0.2%. 4QFY27 PAT stood at INR1,740m, up 346% YoY (est. INR2,075m).

* For FY26, revenue/adj. EBITDA grew 168%/89%, while PAT declined 30% YoY vs. FY25. Our TP of INR340 implies a 34% upside from the current price. We reiterate our BUY rating on the stock, supported by Eternal’s market leadership in both quick commerce and food delivery, and the long-term potential of Blinkit as a generational opportunity in retail, grocery, and ecommerce disruption.

Our view: Assortment, coverage, densification to drive 60%+ NOV CAGR

* The results allay fears of deceleration in quick commerce: Strong growth rebound guidance in 1Q as well as 60%+ CAGR over the next three years, allays market fears around saturation for the quick commerce business. While growth is moderating off a high base (FY23–26 NOV CAGR at ~104%), the commentary suggests demand is still building across cities, with no visible MTU saturation yet. We build in ~70%/65%/50% NOV growth for FY27/28/29E.

* The 100% growth guide for FY27 no longer holds: We believe consensus expectations have already come off, and this should be a positive. Management now hints at ~70% growth in FY27. Competition remains elevated in the near term with different players being aggressive in different regions, though management expects it to ease over the next few years. Importantly, Eternal continues to see stable customer retention and lower CAC (as peers pull back), suggesting that a more rational competitive environment may gradually emerge.

* Three legs of 60%+ NOV CAGR: assortment, coverage, densification; path to USD1b EBITDA by FY29: Assortment expansion (80k SKUs in NCR vs ~20k in smaller cities), geographic expansion (pin code coverage still <30% beyond top cities), and demand densification (low penetration within covered pin codes) remain the three key drivers. Management reiterated the USD1b adjusted EBITDA target by FY29, which implies ~3–3.5% blended QC margins in the medium term, gradually moving toward 5–6% steady-state margins. We estimate EBITDA margins of 1.0%/1.9% for FY27/28E.

* FD NOV recovery encouraging, a result of interventions: FD growth has now accelerated for three consecutive quarters, supported by targeted interventions such as lower MOV (INR 99 for Gold), curated lower ticket offerings, and higher app engagement. While NAOV is declining by design, frequency and order growth are improving, with revenue per order offsetting the mix shift. Management maintains 20%+ YoY NOV growth with 5–6% margins, and we build in ~19% growth for FY27E. We have built in a gradual convergence, with NOV growth of 19.4%/20.0% in FY27/28E.

* Mature stores at 5–6% EBITDA margin; unit economics holding up: Mature markets like NCR are already approaching 5–6% steady-state margins, with 10– 11% contribution margins, indicating strong unit economics at scale. Importantly, profitability in newer cities is tracking closer to mature markets despite lower NAOVs, driven by lower cost structures. While the path may not be linear, given the continued expansion (store count to reach ~3,000 by Mar’27), the underlying store-level economics appear stable. We estimate QC margins at ~1.0% in FY27E, improving to ~3.0% over the medium term.

Valuation and changes to our estimates

* Eternal’s FD business is stable, and Blinkit offers a generational opportunity to participate in the disruption of industries such as retail, grocery, and ecommerce. We largely keep our estimates unchanged. While QC growth is moderating at ~70% in FY27, we see this as a normalization, with improving unit economics and a clearer path to profitability (USD1bn EBITDA by FY29). We factor in gradual margin expansion, led by store maturity and operating leverage. Eternal should report a PAT margin of 2.4%/3.0% in FY27/28E. Our TP of INR340 implies a 34% upside from the current level. We reiterate our BUY rating on the stock.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041