Utilities & Power Equipment : Peak Power Demand Hits 240–244 GW During Daytime By JM Financial Services Ltd

Peak power demand is hovering within 240–244GW during daytime and 200–215GW during evening, and is estimated to bloat to 275–285GW (daytime) and 260–270GW (evening) during the summer. But gas-fired power generation in India during summer is at risk due to disruption in gas production in Qatar. Additionally, all energy (coal, oil, gas) prices are inextricably linked, indicating a possibility of traction in coal prices. On top of this, hydro generation, which can meet 25–28GW during evening, is at risk in CY26 due to more than a 50% deficit in winter rainfall. Hence, there is a high probability of spikes in coal generation to meet evening supplies. We have crafted four scenarios pertaining to extreme uncertainties of fuel supplies (coal, gas) & prices and power demand to get a handle on the fast-changing externalities.

* Gas-fired power generation: India has reduced natural gas allocations to industries by 10% to 30% (and up to 40% for some sectors) as of 4 Mar’26, following a major production halt in Qatar in the wake of escalating tensions involving Iran, Israel and the United States. India has 24,628MW (10,388 private + 7,002 state + 7,238 central) of gas-fired power generation capacity. Currently, it is generating 2.3GW during evening peak, which can go up to 12GW—as seen on 30 May’24 when India recorded highest-ever peak daytime/evening demand of 250GW/233GW (evening). In our view prolonged disruption in gas supplies can cause stress to gas power supply during the upcoming summer at a time when peak daytime/evening demand is estimated to touch 275–285GW/260–270GW. (Exhibit 10 & 11)

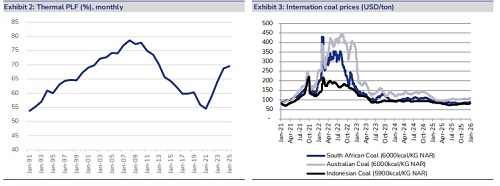

* Inextricably linked energy prices: The level of substitutability of crude oil and coal in production and consumption has always been a subject of discussion among industry players. Empirical results suggest that coal prices are affected by the supply and demand trend of the oil market even though their supply is affected by different dynamics and the two commodities scarcely compete with each other. If oil prices rise with supply constraints, we expect prices of coal in the international market to follow suit, mainly due to the role of substitution, albeit with a little lag, and the regional energy demand-supply matrix. This would be in addition to the recent run-up in Indonesian prices due to a possibility of the government’s mandate for production cuts. (Exhibit 8&9

* When nothing goes right, go left: In recent months, coal power generation (exhibit 2) has been under pressure due to increasing solar generation during daytime and hydro during evening. In 2025, large hydro generation (exhibit 4) grew 15% (157BU to 180BU) at the expense of thermal, which declined 4% (1,392BU to 1,340BU). Large hydro PLF increased from 34% in CY23 to 35% in CY24 and then to 40% in CY25, largely due to variations in seasonal water availability and reservoir levels. But hydro generation during CY26, which can meet 25–28GW during evening is at risk due to more than a 50% deficit in winter rainfall. Furthermore, any shortfall in the 12GW peak gas generation during evening must also be compensated for by increased generation from coal. Hence, there is a high probability of a sharp increase in coal generation to meet evening supplies

* Plausible scenarios: It’s a time of extreme uncertainty. The interplay of fuel (coal and gas) supplies & prices and power demand with an increasing probability (60% as of today) of El Nino can yield varying aggregates for different generation utilities, including Coal India. Enriched with channel checks, we have crafted four scenarios to make better sense of the fast-changing externalities.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361

More News

Defence & Aerospace Sector Update : Revenue softness due to execution timing, but margin & e...