Technology Sector Update : Indian IT: Slow start to the year by Motilal Oswal Financial Services Ltd

Multiple headwinds to demand keep recovery in flux

* We expect demand commentary to stay soft in 1QFY27, as macro, AI and geopolitical overhangs continue to weigh on discretionary spending and decisionmaking cycles. Against this backdrop, we build in tepid QoQ growth across our coverage universe for 1QFY27, with the soft start likely extending into 2QFY27 as well.

* With 1H tracking below the run-rate needed to sustain the upper end of FY27 guidance ranges, the ask on 2H to bridge the gap becomes increasingly impractical. We therefore expect companies to walk back the top end of their guidance bands this quarter. We expect INFO to lower the upper end of its FY27 guidance by 50bp, while HCLT could trim the upper end of its services growth guidance by 100bp.

* 1QFY27 results are likely to mirror this backdrop, with QoQ CC growth expected in the range of -1.5% to 2.0% for large-caps. Mid-caps are expected to outperform once again, with growth ranging from -1.0% to 4.8%, led by continued large-deal ramp-ups. For our coverage universe, we expect aggregate revenue/EBIT/PAT to grow by 14.4%/16.4%/13.3% YoY (all in INR terms). * We expect margins to remain a mixed bag. INFO, HCLT and TECHM are expected to post modest sequential improvement, supported by operating leverage and cost actions. TCS margins may decline due to annual wage hikes, while WPRO, COFORGE, PSYS, and ZENT could see pressure from weaker operating leverage, wage hikes, deal ramp-up costs and continued AI investments. We expect a modest cross-currency headwind of ~20-50bp for most companies.

* Vertical performance in 1Q: BFSI remains the most resilient vertical across our coverage, supported by continued deal ramp-ups and relatively stable spending. Hi-Tech is mixed, with AI-related work offsetting client-specific weakness in parts of the portfolio. Telecom remains soft, while Manufacturing is seeing uneven demand across auto and industrial clients.

* Recent commentary from Accenture (see our note dated 18th Jun’26: Accenture 3QFY26: Continued weak demand) continues to point to slower decision-making and cautious discretionary spending, lending further support to our expectation that demand recovery is likely to remain in flux.

* We cut our target multiples by ~15-20% across most of our coverage (see Exhibit 5) to reflect a slower growth outlook, increasing uncertainty around AI-led productivity, and geopolitical overhang.

* Despite valuations having corrected meaningfully, we believe a sustained rerating will require evidence that demand is improving, revenue growth is stabilizing, and companies can demonstrate that AI-led opportunities are beginning to offset productivity-related headwinds.

Growth expectations across our coverage

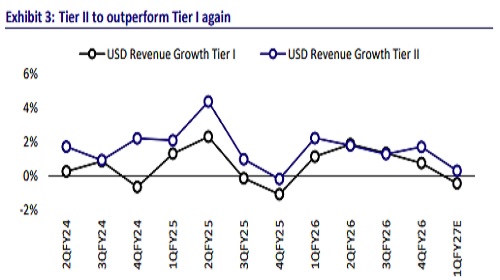

* We expect a mixed 1QFY27 for large-cap IT. TCS and LTM are likely to report flat QoQ CC revenue, while INFO should lead large-cap growth at ~2.0% QoQ CC (organic ~1.0% QoQ CC), supported by acquisitions. Tech Mahindra may deliver ~1.0% growth on telecom deal ramp-ups, whereas HCL Technologies and Wipro are expected to decline due to client-specific issues, delayed ramp-ups and seasonal weakness.

* Among mid-tier firms, we expect HEXT to lead with ~4.8% QoQ CC growth, followed by PSYS (~3.0%), Mphasis and TTL (~2.0% each). Coforge and ZENT are likely to remain flat.

* Among ER&D names, LTTS and TTL should benefit from deal ramp-ups, while TELX is likely to report ~1.2% QoQ CC growth on recovery in Healthcare and Media. Cyient DET is expected to decline ~1.0% QoQ CC as deal conversion remains gradual.

* Cross-currency impact for the quarter: On an average, we expect ~20-50bp crosscurrency headwinds for our coverage on a sequential basis.

Valuations very cheap, but returns may be capped until clarity emerges

* Stocks are now inexpensive, with Tier-I valuations ~30%/40% below their 10- year/5-year averages. TCS and Infosys are trading around -1 SD P/E levels and ~46%/39% below their 10-year averages, while TECHM is trading closer to its 10- year average. We cut our target multiples by ~15-20% across most of our coverage (see Exhibit 5) to reflect a slower growth outlook, increasing uncertainty around AIled productivity, and geopolitical overhang.

* While valuations appear attractive, we believe returns are likely to remain capped until deflationary pressures ease and AI-led implementation use cases begin to scale.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Automobiles Sector Update : MSIL/TMPV outperform in PVs, TVS in 2Ws, and TMCV in CVs by Moti...