Sell Wipro Ltd For Target Rs. 200 by Motilal Oswal Financial Services Ltd

.jpg)

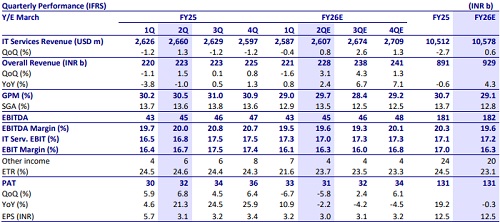

* IT services likely to report 0.3% CC growth, driven by a onemonth inorganic contribution from the Harman acquisition.

* Margins are likely to stay in a tight range (~16.3%), due to upfront requirements in large deal ramp-ups.

* Organically, we expect WPRO to report flat cc growth (midpoint of guidance. Europe is stabilizing from client issues faced; however, recovery is expected to be gradual.

* 2H is expected to outperform 1H, supported by strong deal closures in 1Q. Execution on ramp-ups will be a key monitorable.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

2.jpg)

More News

Healthcare Monthly Sector Update : Acute/Chronic witness highest YoY growth in 24m By Motila...