Neutral ONGC Ltd for the Target Rs. 265 by Motilal Oswal Financial Services Ltd

Production volume growth disappoints

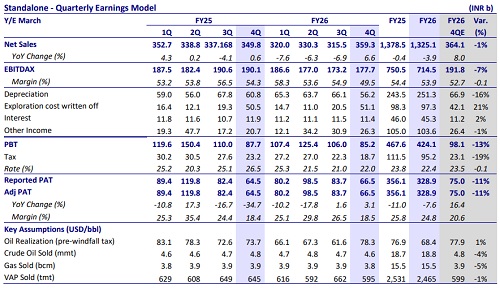

* ONGC’s 4QFY26 standalone revenue came in line with our est. at INR359b. Crude oil/gas sales were 4%/5% below our est. at 4.6mmt/3.8bcm. Reported oil realization was USD78.3/bbl. Crude oil production declined 3%/6% QoQ/YoY, and natural gas production declined 4%/3% QoQ/YoY. Weakness in oil production was attributed to 1) geological complexities at the 98/2 field in the Eastern offshore, and 2) operational issues at the DUDP project. SA EBITDAX came in 7% below our est. at INR178b. Other expenses were above our est. Exchange loss stood at INR11.8b in 4QFY26. SA APAT stood 11% below our est. at INR67b.

* Key things we liked about the result: 1) ONGC has extended the technical service provider contract to cover the entire Western Offshore after a promising outcome in the Mumbai High field. 2) OPaL’s performance improved as it reported a loss of INR0.7b in 4QFY26 (vs. a loss of INR5.4b/ INR13.3b in 3QFY26/4QFY25). OPAL faced some temporary operational issues in Mar’26, including gas diversion towards LPG, affecting production and earnings. Management remains confident of a turnaround as overseas assets stabilize and new projects ramp up. 3) New well gas contribution continues to ramp up, with production already above 9mmscmd from Apr’26 and another ~3mmscmd expected via Daman Upside. NW gas now contributes ~25% of ONGC’s gas output (vs. 17% earlier) and is expected to rise to ~30% in FY27 and ~34-36% by FY28. 4) Under “Project DeepX” and the “Samudra Manthan” initiative, ONGC plans to double deepwater drilling activity over the next two years, intensifying focus on frontier exploration.

* Key investor concerns: 1) Crude oil production declined 3%/6% QoQ/YoY, while natural gas production fell 4%/3% QoQ/YoY, largely due to geological complexities at the 98/2 field in the Eastern offshore and operational issues at the DUDP project. 2) Due to reservoir complexities, KG 98/2 is currently producing ~24kb/d of oil and 2.3mmscmd of gas, with management expecting production to recover to earlier levels of 25- 30kb/d oil and 3-4mmscmd gas over the next year. ONGC could see soft production volumes in 1HFY27.

* Valuation and view: We reiterate our Neutral rating on the stock and arrive at our SoTP-based TP of INR265 as we model a CAGR of 2.7%/3.7% in oil/gas production volumes over FY26-28.

APAT miss due to high dry-well write-offs

* In 4QFY26, ONGC’s revenue came in line with our est. at INR359b.

* Crude oil/gas sales came 4%/5% below our est. at 4.6mmt/3.8bcm. VAP sales stood at 595tmt (est. 599tmt).

* Reported oil realization was USD78.3/bbl.

* Crude oil production declined 3%/6% QoQ/YoY, while natural gas production declined 4%/3% QoQ/YoY.

* Weakness in oil production was attributed to 1) geological complexities at the 98/2 field in the Eastern offshore, 2) operational issues at the DUDP project.

* EBITDAX came in 7% below our est. at INR178b.

* Other expenses stood above est. Exchange loss stood at INR11.8b in 4QFY26.

* ONGC booked additional impairment at Mozambique (INR2.1b) and Sakhalin (INR5b) assets in 4QFY26.

* APAT stood 11% below our estimate at INR67b.

* Dry well write-offs were above our est. Finance costs and other income stood in line with our estimate.

* ONGC has extended the technical service provider contract to cover the entire Western Offshore after a promising outcome in the Mumbai High field.

* ONGC Videsh:

* OVL’s oil and gas production was down YoY at 1.74mmt/0.77bcm (1.86mmt/0.81bcm in 4QFY25).

* Crude oil sales stood at 1.05mmt, while gas sales came in at 0.35bcm.

* OVL’s revenue (incl. other income) was INR44.4b, and PBDT stood at INR30.8b.

* ONGC Petro additions Limited (OPaL):

* OPaL’s average capacity utilization for 4QFY26 stood at 93% (vs 85%/95% in 3QFY26/4QFY25).

* OPaL reported a loss of INR0.7b in 4QFY26 (vs. a loss of INR5.4b/INR13.3b in 3QFY26/4QFY25).

* The Board declared a final dividend of INR1/sh (interim dividend: INR12.25/sh) (FV: INR5/sh).

Valuation and view

* In the past few quarters, ONGC has struggled to raise production/sales, with no meaningful production/sales growth YoY in FY26. Further, we like the increased exploration intensity (which is key to building a robust development pipeline), though we believe it will likely be accompanied by higher dry well write-offs, which will weigh on earnings. Further, the benefits of an increased new well gas proportion for ONGC will be mostly offset by subdued gas realization amid a weaker crude oil price outlook.

* We arrive at our SoTP-based TP of INR265 as we model a CAGR of 2.7%/3.7% in oil/gas production volume growth over FY26-28.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)