2026-01-10 04:31:45 pm | Source: Motilal Oswal Financial Services Ltd

Neutral Nestle India Ltd for the Target Rs. 1,300 by Motilal Oswal Financial Services Ltd

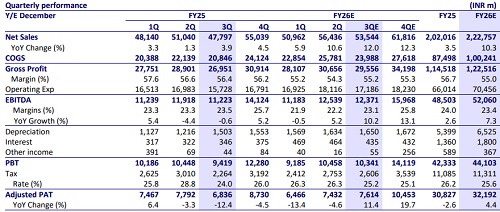

* We model 12% YoY consol. revenue growth. Domestic business is expected to grow 12% led by volume. The growth is supported by the normalization of trade post-GST implementation.

* NEST has been strategically taking pricing action in response to rising commodity prices.

* We expect GP margin contraction of 120bp YoY, but it has expanded 90bp QoQ to 55.2% due to the moderation in RM prices sequentially. EBITDA margin to contract by 40bp YoY to 23.1%.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Disclaimer:

The content of this article is for informational purposes only and should not be considered financial or

investment advice. Investments in financial markets are subject to market risks, and past performance is

not indicative of future results. Readers are strongly advised to consult a licensed financial expert or

advisor for tailored advice before making any investment decisions. The data and information presented

in this article may not be accurate, comprehensive, or up-to-date. Readers should not rely solely on the

content of this article for any current or future financial references.

To Read Complete Disclaimer Click Here

Latest News

Global oil demand recovery underway, peace in Gulf m...

Hybrid long?short funds dominate SIF AUM with nearly...

Bank deposit surge in India indicates stronger capit...

Commerce Secretary calls for predictable policy to a...

Stakeholders deliberate on 3 key pillars for impleme...

Nifty, Sensex post mild weekly loss over escalating ...

FIIs turn net buyer this week, purchase Rs 4,670 cro...

Private Credit Emerging as Mainstream Asset Class in...

Buy Tata Consultancy Services Limited for the Target...

SIF AUM surges 29% to Rs 17,858 crore in June; Hybri...