Neutral Mphasis Ltd For Target Rs. 3,000 by Motilal Oswal Financial Services Ltd

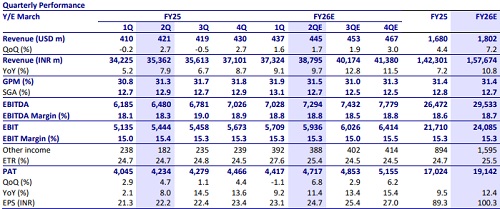

* We expect 1.5% QoQ CC growth, aided by ramp-up in BFSI and TMT verticals. However, steady TCV-to-revenue conversion is key to tracking execution from hereon.

* Expect notable improvement in TCV win rate in FY26; this could improve growth visibility for the next 4-6 quarters.

* Margin is likely to be flat, with utilization to hold steady and no material change in amortization or SG&A ratios. EBIT margin to be within guided band of 14.75-15.75%.

* Commentary around demand environment, volume recovery for its mortgage business, deal TCV & revenue conversion and logistics vertical will be worth tracking.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412