Neutral HDFC Life Insurance Ltd for the Target Rs.760 by Motilal Oswal Financial Services Ltd

VNB margin below est. at 24%

* HDFC Life Insurance (HDFCLIFE) reported an APE of INR52.5b (in line) in 4QFY26, up 1% YoY, with individual APE flat YoY and group APE growing 10% YoY. For FY26, APE grew 8% YoY to ~INR166.4b.

* VNB declined 8% YoY to INR12.6b (in line), resulting in a VNB margin of 24% vs. 26.5% in 4QFY25 (est. 24.8%). For FY26, VNB grew 2% YoY to INR40.3b, leading to a VNB margin of 24.2% (25.6% in FY25).

* EV as of FY26 end was at INR621.4b (up 12% YoY), with operating RoEV of 15% for the year.

* HDFCLIFE is entering FY27 with a largely completed GST transition, a supportive yield curve, improving agency channel, and a strengthening protection portfolio. The insurer aspires to outpace industry growth in APE and expects VNB growth to be better than APE growth.

* We maintain our premium estimates but cut our VNB margin estimates by 150bp/100bp for FY27/28, considering the 4QFY26 performance and with operating RoEV near 15%. We reiterate our BUY rating with a revised TP of INR760 (based on 2x FY28E EV).

Non-par savings slow down, but protection share rising

* For 4QFY26, HDFCLIFE’s gross premium grew 10% YoY to INR264b (in line), driven by 14% YoY growth in renewal premium and 8% YoY growth in single premium.

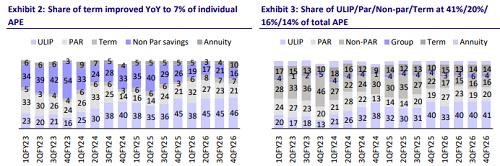

* Protection segment witnessed strong growth of ~42% YoY, driven by GST exemption, while ULIP and Par segments grew in single digits. Non-par savings APE declined ~26% YoY, and management expects the momentum to improve as yield curve turns favorable.

* Contribution from protection segment continued to improve YoY, with individual protection contributing 7% to APE in 4QFY26 (3% in 4QFY25) and additional 3% contribution coming from riders.

* While the rising share of protection and improving ULIP margins were beneficial for VNB margin, it was impacted by loss of ITC (110bp), which is expected to taper down and stabilize by 1HFY27.

* On an individual APE basis, the agency channel witnessed strong growth of 19% YoY, backed by continued investment toward productivity improvement. Broker/direct channel grew 13%/23% YoY, while banca channel witnessed a slowdown (+5% YoY) owing to heightened competitive intensity.

* Persistency ratios declined YoY across 13M/25M/49M in 4QFY26. 37M and 61M persistency improved YoY, and management is working on various persistency improvement initiatives.

* As of Mar’26, total AUM grew 12% YoY to INR3.8t.

* EV as of FY26 end was at INR621.4b (+12% YoY), reflecting operating RoEV of 15% for the year. Solvency ratio stood at 177%, with a 900bp increase expected due to INR10b worth of preferential shares issued to HDFC Bank.

* Commission ratio declined to 10.5% from 10.7% in 4QFY25, and opex ratio increased to 10.7% from 9.5% in 4QFY25, resulting in a rise in overall expense ratio to 18.6% from 17.9% in 4QFY25.

Highlights from the management commentary

* FY26 performance was below management’s expectations. While 1HFY26 was ahead of the industry and 3Q met expectations, 4Q saw a slowdown due to the unabsorbed GST impact and demand deferment in Mar’26. Management remains confident of a rebound, supported by strong customer acquisition, with ~70% of customers onboarded during the year being first-time buyers of HDFC Life.

* Annuity segment saw meaningful progress. A new product launched in 4QFY26—an industry-first variable annuity linked to the Nifty 50 index— supported growth and contribution. Product mix is expected to shift toward non-par savings, while annuity and protection are likely to grow faster than overall company growth.

* Margin compression was driven by GST and surrender value changes (-130bp), fixed cost absorption (-90bp), and strengthening of persistency assumptions (- 40bp), partially offset by product mix shift (+120bp).

Valuation and view

* HDFCLIFE has witnessed a slowdown in growth at the end of 2HFY26. However, some green shoots were witnessed with respect to improvement in agency channel growth, rising protection contribution and improving ULIP margins. We expect the growth trajectory to improve, along with a stable VNB margin, driven by a diversified product mix, rising sum assured (especially in ULIPs), and improving rider attachments. While the loss of ITC has impacted profitability, the same is likely to be fully absorbed by 1HFY27, normalizing its VNB margin while maintaining a strong position in the industry.

* We maintain our premium estimates but cut our VNB margin estimates by 150bp/100bp for FY27/28, considering the 4QFY26 performance and with operating RoEV near 15%. We reiterate our BUY rating with a revised TP of INR760 (based on 2x FY28E EV).

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

.jpg)