Neutral Escorts Kubota Ltd for the Target Rs. 3,159 by Motilal Oswal Financial Services Ltd

New launches to help drive market share revival

Modest outlook given macro challenges

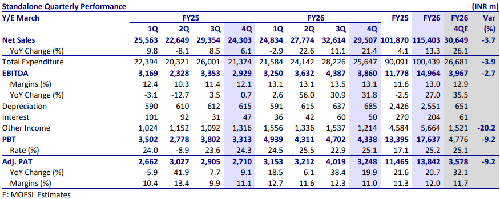

* Escorts’ 4QFY26 PAT at INR3.2b came in below our estimate of INR3.6b due to lower other income, while EBITDA was broadly in line with our estimate. Tractor margins disappointed, whereas Construction Equipment margins surprised positively.

* Market share loss in tractors over the last couple of years remains the key investor concern in Escorts. Further, synergies between Escorts and Kubota are significant, which will likely materialize over the medium to long term. The stock at ~28.4x/25.7x FY27E/FY28E EPS appears fairly valued. We reiterate our Neutral rating on the stock with a TP of INR3,159, based on ~24x FY28E EPS.

Earnings miss due to lower-than-expected other income

* Escorts’ 4Q standalone revenue came in slightly below our estimate at INR29.5b (est. ~INR31b), growing 21.4% YoY (-9.5% QoQ). Though tractor volumes were up by 21.1% YoY to ~32k units, average realizations were flat YoY due to an adverse product mix.

* EBITDA margin improved 100bp YoY to 13.1% (-40bp QoQ), slightly above our estimate of 12.9%. Operating leverage benefit drove margin improvement.

Tractor margin was broadly flat YoY at 11.3% (below estimated 13%). Construction equipment margin improved 360bp YoY to 12.7 (above estimated 6.1%).

* EBITDA grew 31.8% YoY to INR3.9b (broadly in line).

* Other income at INR1.2b was lower than our estimate. ? As a result, PAT came in below our estimate at INR3.2b, up 19.9% YoY.

* For FY26, revenue/EBITDA/PAT rose 17.9%/27%/46.8% YoY to INR115.4b/INR15b/INR13.8b.

* In FY26, CFO stood at INR13.8b and FCF was healthy at INR10.7b. FY26 ROE/ROCE were up to 11.9%/15.9%.

Highlights from the management commentary

* Market share loss of Escorts in FY26 is largely attributable to regional demand skew, wherein its core North and Central markets grew relatively slower at 15-17% compared to West and South, which posted healthy 30% growth.

* Management expects tractor industry demand to moderate to a flat trajectory (±2-3%) in FY27, citing a high base, weaker reservoir levels, emerging El Niño risks, and commodity-led affordability pressures. However, EKL expects to outperform industry growth through new launches, improved channel readiness and stronger financing support.

* Management expects component exports into Kubota’s global supply chain to ramp up meaningfully over the medium term, targeting INR5- 10b of component exports from India by FY30.

* Margin outlook for FY27 remains mixed. Input costs have surged, especially for steel, tyres, copper, aluminum, energy and labor. Wage inflation in key manufacturing regions like Haryana and Uttar Pradesh is likely to create a structural cost increase. These cost pressures will be partially offset by calibrated price hikes (~1.5% taken in April), productivity initiatives and ongoing cost rationalization.

* Capex guidance for FY27 stands at INR3.5-4.0b for the core business. Apart from this, EKL intends to invest INR5b in the new greenfield facility. Total investments for phase 1 of this facility are expected to be INR20b, with about INR70b+ planned as investments over the next 7-10 years.

Valuation and view

* Market share loss in tractors over the last couple of years remains the key investor concern in Escorts. Further, synergies between Escorts and Kubota are significant, which will likely materialize over the medium to long term. We factor in Escorts to post a CAGR of 7%/4%/9% in revenue/EBITDA/PAT over FY26-28E. The stock is trading at ~28.4x/25.7x FY27E/28E EPS, which is at a significant premium to its 10-year average of ~20x, mainly due to the Kubota parentage. Given that most of the positives seem to have already been factored into valuations, we reiterate our Neutral rating on the stock with a TP of INR3,159, based on ~24x FY28E EPS.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412