Neutral Eicher Motors Ltd for the Target Rs 6,912 by Motilal Oswal Financial Services Ltd

Steady quarter Domestic demand remains healthy, exports uncertain

* Eicher Motors (EIM)’s 4QFY26 consolidated PAT at INR15.2b was largely in line. RE and VECV both performed in line with our expectations, and both entities are showcasing EBITDA margin expansion YoY.

* We project RE to record a 13.5% volume CAGR over FY26-28. However, while we expect the domestic business to deliver a 14% CAGR, exports are likely to post a much slower CAGR of 9%, that too largely back-ended.

* Given management’s focus on volume growth and the recent upsurge in input costs, we expect margins to remain under pressure. Overall, we expect EIM to post a 14% earnings CAGR. At 31.6x/27.6x FY27E/FY28E, the stock appears fairly valued. Reiterate Neutral with a TP of INR6,912. We value RE at 28x FY28E EPS and VECV at 12x EV/EBITDA.

Earnings in line for both RE and VECV

* Eicher's consolidated revenue grew 16% YoY to INR60.8b (in line), aided by strong volume growth from the RE and VECV businesses. RE realizations were marginally higher YoY at INR186k (+3%), while VECV realization declined ~2% YoY in 4Q.

* Consolidated EBITDA margin grew 90bp YoY to 24.9% (down 60bp QoQ) and was in line.

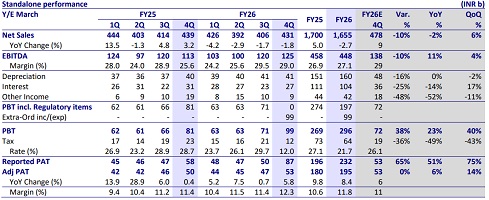

* Standalone margin improved 110bp YoY to 25.8%, led by operating leverage benefits. Standalone PAT was up 9.9% YoY to INR12.3b, in line.

* EBITDA margin at VECV remained broadly flat YoY at 10.4% (below our estimate of 10.8%). VECV’s recurring PAT grew 23.4% YoY to INR5.6b, in line with our estimate.

* Recurring PAT for the consolidated entity grew ~12% to INR15.2b (in line).

* For the full-year FY26, revenue/EBITDA/PAT for the entity grew by 24%/23%/17% YoY to INR234b/INR57.9b/INR55.5b.

* For the year, CFO improved to INR48b while FCF was positive at INR35.4b.

* The Board has declared a final dividend of INR82/share for the year FY26, translating to a dividend payout of ~41%. This was stable YoY.

Valuation and view

We project RE to record a 13.5% volume CAGR over FY26-28E. However, while we expect the domestic business to deliver a 14% CAGR, exports are likely to post a much slower 9% CAGR, that too largely back-ended. Given management’s focus on volume growth and the recent upsurge in input costs, we expect margins to remain under pressure. Overall, we expect EIM to post a 14% earnings CAGR. At 31.6x/27.6x FY27E/FY28E, the stock appears fairly valued. Reiterate Neutral with a TP of INR6,912. We value RE at 28x FY28E EPS and VECV at 12x EV/EBITDA.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Tag News

NDR Auto Components surges as its arm inaugurates new plant in Andhra Pradesh