Neutral Bharat Forge Ltd for the Target Rs. 1,835 by Motilal Oswal Financial Services Ltd

Strong guidance in a weak macro is encouraging

Defense order execution remains the key monitorable

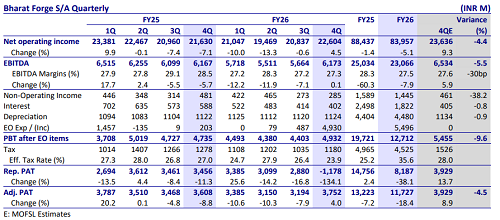

* Bharat Forge’s (BHFC) 4QFY26 standalone adjusted earnings at INR3.7b came in slightly below our estimate of INR3.9b due to lower-thanexpected revenue and an adverse mix.

* The GST rate cut has helped revive the domestic auto business, which augurs well for BHFC. Further, the US Class8 cycle appears to have bottomed out now, with early signs of revival. Defense, aerospace, and JSA are likely to remain the key growth drivers for BHFC in the coming years. We now expect BHFC to post a CAGR of 16%/22%/39% in revenue/ EBITDA/PAT over FY26-28E. However, following the recent rally in the stock, most positives seem to be factored in (valuation now at 55.9x FY27E EPS and 41.2x FY28E EPS). Reiterate Neutral with a TP of INR1,835 per share (valued at 38x FY28E EPS).

Earnings below estimates due to weak demand and adverse mix

* 4Q standalone revenue rose 4.5% YoY to INR22.6b (slightly below est. of INR23.7b). Volumes declined 8% YoY to 62,201MT, while realizations grew 13.1% YoY to INR363/kg.

* Auto revenue declined 7.1% YoY to INR10.6b (slightly above estimate), whereas non-auto revenue grew 17.5% YoY to INR12.1b (missing estimate of INR13.4b).

* Export revenue at INR10.8b declined ~12% YoY but improved QoQ mainly due to a combination of inventory restocking and a rebound in NA truck production volumes after the cyclical bottom seen in 3QFY26. On the other hand, domestic CV revenue was strong, driven by high production volumes across OEMs. Overall domestic revenue grew 32% YoY to INR10.6b.

* Standalone EBITDA margins declined 120bp YoY to 27.3% vs. est. of 27.6% due to an adverse mix. EBITDA, however, was flat YoY at INR6.2b (missing estimate of INR6.5b).

* There was an exceptional expense of INR4.9b as a provision for impairment of investment in KPTL.

* Adjusted for this expense, PAT fell 28.7% YoY to INR2.6b, missing our estimate by ~35%.

* Consolidated revenue rose 17.5% YoY to INR45.3b, while consolidated margins were down 50bp YoY at 17.2%.

* Overseas subsidiaries’ margins improved to 3.7% in 4Q from 1.2% YoY, led by improved utilization. Europe subsidiaries’ margin improved 350bp YoY to 4.7%, and US subsidiaries’ margin fell marginally YoY by 20bp to 1.1%.

* For FY26, revenue/EBITDA/PAT grew 11%/9%/18% YoY. Further, FCF for FY26 improved to INR3.7b after capex of INR11b.

Highlights from the management interaction

* For FY27, barring any major geopolitical disruption, management remains optimistic of delivering ~25% revenue growth in Indian manufacturing operations with commensurate improvement in EBITDA and profitability, supported by strong order execution, export market recovery and healthy demand conditions in both India and the US.

* Within the portfolio, growth is expected to be led by Aerospace, followed by Defense and Auto Components.

* The defense order book stood at INR110b at FY26-end, providing strong multiyear revenue visibility. Upcoming key milestones include ATAG production ramp-up and CQB carbine commercialization, which are expected to meaningfully contribute to defense revenue from 2HFY27 onward.

* Aerospace revenue stood at INR4b in FY26, and management expects strong double-digit growth in the segment going forward - well ahead of overall company growth, driven by rising global outsourcing, new program wins and increasing wallet share with marquee aerospace OEMs.

* CV exports remained under pressure through much of FY26 due to channel destocking in North America. However, early signs of recovery emerged in 4Q, and management expects gradual normalization in FY27, supported by inventory restocking and higher production schedules.

* In the recently acquired K-Drive entity, management sees potential for this axle business to scale ~2x over the next 3-4 years while targeting healthy mid-teen operating margins over the medium term.

Valuation and view

The GST rate cut has helped revive the domestic auto business, which augurs well for BHFC. Further, the US Class8 cycle appears to have bottomed out, with early signs of revival. Defense, aerospace, and JSA are likely to remain the key growth drivers for BHFC going forward. We expect BHFC to post a CAGR of 16%/22%/39% in revenue/EBITDA/PAT over FY26-28E. However, after the recent rally in the stock, most positives seem to be factored in (valuation now at 55.9x FY27E EPS and 41.2x FY28E EPS). Reiterate Neutral with a TP of INR1,835 (valued at 38x FY28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412