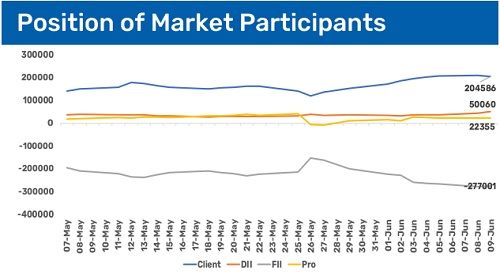

Morning Bell 10th June 2026 by Bajaj Broking Ltd

Market Commentary

Indian benchmark indices witnessed a volatile session on 09 th June, the Nifty weekly expiry day, but managed to close on a positive note . The recovery was primarily supported by easing crude oil prices and strength in the Indian Rupee, which improved overall market sentiment and triggered strong buying interest in banking stocks . As a result, the banking sector emerged as the key driver of the market's gains, with the Nifty PSU Bank Index rallying 3.62 % and the Nifty Private Bank Index advancing 1.64 % during the session .

* At the close, the Sensex gained 394 .50 points (0 .54 %) to settle at 73 ,918 .76 , while the Nifty advanced 119.10 points (0 .52 %) to close at 23 ,242 .10.

* On the sectoral front, buying interest remained broad - based, with major support coming from Nifty PSU Banks, Private Banks, Realty, and Auto stocks . On the other hand, Nifty IT and Media emerged as the key underperformers and closed in negative territory .

* Gift Nifty signals a negative opening for the Indian market . Nifty spot in today's session likely to trade in the range of 23 ,000 - 23 ,400 .

Global Updates

* Wall Street closed out Tuesday's mixed session on a highly volatile, bifurcated note . While small - caps and traditional value sectors managed minor positive holds, large - cap technology distribution restricted any broad index upside .

* Wall Street's technology basket faced fresh downward pressure on Tuesday . Apple shares dropped over 3.6% after its annual developer conference (WWDC) presentations on "Apple Intelligence" and Siri AI features left investors feeling underwhelmed . Institutional desks are raising near -term concerns over hardware limitations and the actual timeline for upgrade monetization, pulling the Nasdaq lower .

* Asian regional layouts are deeply divided this morning, with tech - heavy export centres feeling the direct heat of Wall Street’s chip and software pullback :

Above views are of the author and not of the website kindly read disclaimer

.jpg)