Monthly Auto Sales - October 2025 by ARETE Securities Ltd

The auto sector experienced a steady 1% MoM and 5% YoY growth in October, driven by strong performances across key segments especially PV segment which grew 19% MoM and 13% YoY. The PV segment led the growth, supported by festive season demand, GST rate cuts, and promotional discounts,with MSIL leading the charge and TAMO gaining traction in domestic markets. In contrast, HMIL faced a dip in annual volumes, likely due to inventory build-up ahead of the season. The CV segment also posted healthy gains, driven by robust demand for LCVs, which saw a significant uptick, particularly in the e-commerce sector, with AL leading in this space. Trucks also performed well, supported by a surge in infrastructure projects and strong contributions from M&M. In the 2W segment, domestic volumes faced challenges, with HERO's performance dragging down the overall results,though other players like TVS showed positive growth. The tractor segment maintained its positive trend with a sequential rise in domestic volumes,driven by favourable agricultural conditions,festive retail activity, and expectations of strong Rabi sowing and Kharif harvesting. The auto sector may experience a deceleration in coming months as the festive and policy-driven boost fades, with growth prospects depending on affordability, broader 1% decline YoY, HMIL was the exception, it posted an 11% YoY growth, following its focus on export expansion. economic conditions, and seasonal factors.

Automobile Sales October - 2025

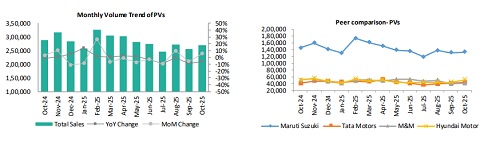

PV Segment

The PV segment experienced a notable 19% MoM and 13% YoY surge in dispatch volumes this month, driven by industry-wide GST rate cuts and promotional discounts on various car models amid the festive season. MSIL led the growth with a strong 29% MoM increase, benefiting from robust demand across its portfolio. The Mini segment, in particular, saw its highest sequential growth of the fiscal year, contributing to this overall uplift. TAMO gained strong traction in domestic markets, while HMIL, despite a sequential rise, saw an annual dip, likely due to its strategy of consecutively building dealer inventory over the last three months for the festive season, which reduced the need for immediate dispatches. M&M regained its position as runner-up after two months, buoyed by the launch of refreshed versions of its key SUV models: the Thar, Bolero, and Bolero Neo. Exports this month, however, saw a dip of 24% MoM across most companies and a 1% decline YoY, HMIL was the exception, it posted an 11% YoY growth, following its focus on export expansion.

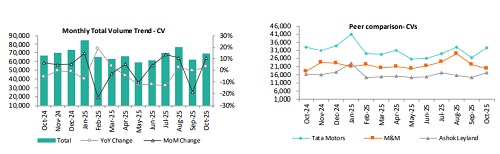

CV Segment

The CV segment experienced a robust 8% MoM and 10% YoY increase in overall volumes in October, fuelled by factors such as the festive season, GST rate revisions, and an uptick in demand for LCVs, which contributed 21% of the segment's total volume, rising 7% MoM and 13% YoY. The e-commerce sector played a key role in driving LCV demand, with AL leading the growth in this space. Domestic truck volumes reached fiscal peak levels, supported by a surge in infrastructure activities post-monsoon, rising 8% MoM and 11% YoY, with M&M showing a significant 35% MoM and 16% YoY growth. However, the bus segment saw more muted growth, with a 1% MoM increase and a strong 19% YoY rise. Notably, TAMO, the volume leader in the bus category, drove the annual growth, posting a 3% MoM and 12% YoY increase, while AL and M&M saw little change in their respective volumes.

.

.

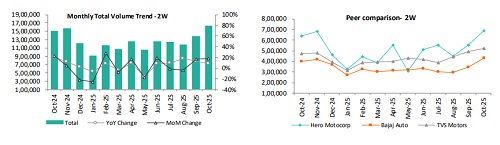

2W Segment

The 2W segment faced a challenging month, with a 2% MoM decline and a 2% YoY rise, largely driven by HERO's weak performance, which saw volumes fall by 7% MoM and 6% YoY, potentially due to its strategy of pushing dealer inventory ahead of the festive season and a slight shift noticed amongst existing 2W owners toward PVs, driven by recent price cuts making cars more affordable for aspirational buyers. In the domestic market, TVS stood out with the best growth in percentage terms, and while HERO underperformed, most other players posted positive annual growth. On the export front, BAJAJ, the export segment leader, posted solid growth with a 12% MoM and 11% YoY increase in volumes, but other export players struggled sequentially, limiting overall 2W export growth to just 1% MoM, although exports still showed a significant 16% YoY growth.

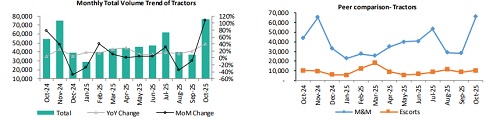

Tractor Segment

Tractors posted a positive volume uptick for the third consecutive month, rising by 10% MoM and 11% YoY, driven primarily by domestic dispatches, which surged 9% MoM. This growth was supported by increased retail activity of the festive season, consistent government support, and favourable agricultural conditions, including ample water levels in reservoirs. Moving forward, demand is expected to remain strong as Rabi sowing starts on time and Kharif harvesting progresses well. In the domestic market, M&M, the market leader, saw a double-digit surge in volumes, while ESC experienced more modest growth with just 3% increases on both MoM and YoY bases. On the export front, volumes grew significantly by 21% MoM and 40% YoY, again led by M&M, reflecting strong demand in international markets.

Please refer disclaimer at http://www.aretesecurities.com/

SEBI Regn. No.: INM0000127