Monthly Auto Sales - March 2026 by ARETE Securities Ltd

.jpg)

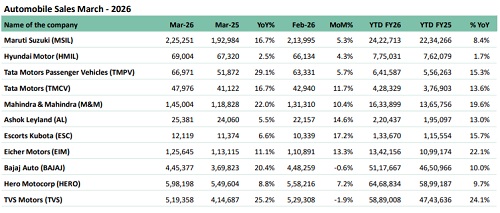

Auto dispatches increased 3% MoM and 16% YoY in March, with broad-based domestic growth, while exports grew 20% YoY but declined 8% MoM with ~21% mix. 2Ws led the growth, supported by rural demand recovery and fiscal-end push, while PVs saw stable traction with MSIL, M&M and TMPV contributing. CVs improved across segments with TMCV, AL and EIM driving volumes, particularly in trucks and buses. Tractor demand remained strong domestically due to seasonal tailwinds, even as exports lagged. Despite the typical March boost, FY26 performance was marked by better demand consistency, especially in 2Ws, alongside steady gains in PVs and CVs, suggesting a more durable recovery compared to the volatility seen in previous periods.

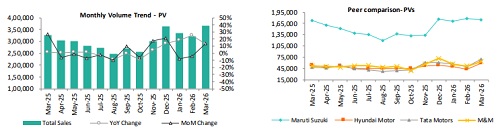

PV Segment

Domestic PV dispatches rose 3% MoM and 15% YoY, with broad-based growth across OEMs, supported by festive demand, year-end dealer push and targeted discounting, particularly in EVs by M&M and TMPV. MSIL led volume growth, while HMIL retained its fourth position. Export volumes increased 15% MoM and 27% YoY, again led by MSIL. For FY26, PV volumes grew 7% YoY, driven primarily by M&M, supported by its SUV portfolio and incremental contribution from new launches such as BE6, XEV9e and 9S.

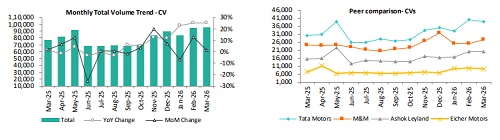

CV Segment

CV dispatches rose 13% MoM and 11% YoY, with growth led by TMCV across both domestic and export markets. Trucks, contributing 65% of volumes, grew 11% MoM and 14% YoY, with EIM posting the fastest growth while M&M saw the highest incremental contribution. LCVs (18% mix) increased 9% MoM and 11% YoY, driven by TMCV. Domestic buses (14% mix) rose 48% MoM and 5% YoY, albeit on a lower base, with TMCV leading. For FY26, industry volumes grew ~10% YoY across most OEMs, with AL lagging but broadly in line.

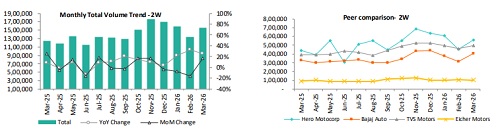

2W Segment

March volumes rose 3% MoM and 16% YoY, supported potentially by rural recovery, fiscal-end push, festive activities and some discounting on key models. E2W demand picked up ahead of subsidy cuts, with TVS/BAJAJ/HERO at 49.3k/46.2k/21.4k units, up 60%/ 31%/167% YoY. For FY26, growth was driven by steady improvement in monthly volumes rather than one-off events. Volumes stayed largely above ~9.5 lakh/month, with fewer weak months, showing better demand consistency. TVS led growth with strong domestic volumes and matching export traction, while BAJAJ and HERO saw stable growth. Overall, trends indicate gradual demand recovery rather than festival-led spikes.

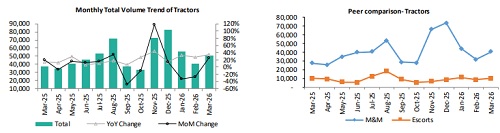

Tractor Segment

Domestic tractor dispatches rose 23% YoY, driven by harvest season activity in northern India and the full-month Chaitra Navratri festival, with FY-end channel stocking supporting a 29% MoM increase. Seasonal factors, including improved rabi crop outlook and reservoir levels, contributed to sustained farmer demand. In contrast, exports accounted for 4% of total volumes, declining 16% MoM and 26% YoY across the industry, reflecting subdued overseas orders and a higher domestic focus. Overall, domestic strength offset weak export trends, with monthly sequential gains largely supported by timing of festival demand and channel inventory adjustments.

Please refer disclaimer at http://www.aretesecurities.com/

SEBI Regn. No.: INM0000127