Logistics Sector Update : Freight and cargo monthly by Emkay Global Financial Services Ltd

We monitor monthly indicators for assessing freight and cargo movements across multiple modes of transportation. Pent up demand, owing to GST rate cuts and pre-festive season, seems to have petered out in Oct-25 as GST e-way bill volumes declined sequentially (-4% in Oct-25/-1% on a 3M rolling average basis). However, lead indicators like manufacturing PMI suggest volumes are likely to remain healthy going ahead. Truck freight rates and diesel prices have been stable for the past two quarters despite volatility in freight volumes. Volume at major ports continued to witness double-digit growth on a YoY basis for two consecutive months (+12/4% YoY/MoM in Oct-25) led by growth across key commodity segments (POL: +16% YoY; Coal: +22% YoY, container volume: +12% YoY). Container shipping rates have now recovered from a 20- month low in Oct-25, up 6% MoM as on 20-Nov-2025, although they are still ~70% below the highs seen in Jul-24, amid continued geopolitical uncertainties

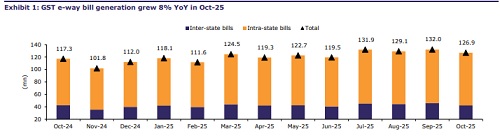

GST e-way bill volumes moderate; freight rates stable

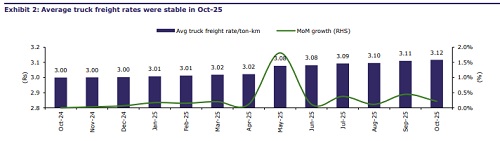

GST e-way bill volumes moderated in Oct-25 (+8% YoY / -4% MoM), as the pent-up demand from pre-festive season and GST rate-cuts lost steam, in addition to an unfavorable base (festive season was in Nov last year). Intra-state volumes were down 2% MoM (up 13% YoY), while inter-state volumes fell 8% MoM and 1% YoY, respectively. We anticipate volume growth will remain healthy going forward on the back of positive trends sustaining in the manufacturing PMI (at 59.2; up by ~150bps MoM in Oct-25). Despite the volatility in volumes, average freight rates on trunk routes were flat sequentially, albeit up 4% YoY (flat on a 3M rolling average basis). Media articles suggest that the government has increased the cost of vehicle fitness tests for older vehicles by up to 10x (Link), which is likely to lead to freight hikes ahead, especially on intra-state routes where higher number of aged trucks ply. Diesel prices have been flat since May25, while ATF prices have grown 4% YoY. Brent crude, meanwhile, has seen a 5% MoM decline in Oct-25

Volume uptick continues at major ports

In Oct-25, volume growth remained robust, up 12% YoY and up 8.6% YoY on a 3M rolling average basis vs FY25 growth of 4.3%. Container volume growth was in line with total ports volume growth, increasing 13% YoY. Despite this momentum, APSEZ continues to outpace industry growth, with container volumes growing 24% YoY in Oct-25 (FY25 growth: 22%). In terms of commodities, coal saw a 22% YoY growth, with both thermal and coking coal growing YoY at 13% and 47%, respectively, highlighting strong demand for energy generation. POL/Fertilizers too contributed to the growth, increasing 16%/85% YoY. Iron volumes witnessed another month of decline – down 2% YoY. Among major ports, Kandla, JNPT, and Visakhapatnam saw the strongest YoY volume growth, of 19%, 11%, and 9%, respectively. JNPT’s market share in containers remains rangebound, awaiting an uptick once WDFC is fully commissioned.

Container shipping rates showing signs of recovery

Per the Drewry WCI Index, container shipping rates have remained under pressure since the announcement of US tariffs. However, from the lows seen in Oct-25, shipping rates are up 6% MoM in Nov-25 (USD1,852 per 40ft container, as on 20-Nov-25). Industry reports suggest that freight rates are likely to recover in the coming period, with normalization of trade demand, diligent capacity management by carriers, and escalating port congestion.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354

More News

Automobiles Sector Update : Auto Sales Soar as Rain Pours by PL Capital