IT Sector Update : Broad-Based Stability led by FX Tailwinds Despite Macro Concerns by Choice Institutional Equities

Q4FY26E Likely to Benefit from FX Tailwinds and Execution Stability

IT services companies are likely to report a resilient Q4FY26E, aided by the reversal of furloughs, stable deal ramp-ups, continued vendor consolidation, and a healthy AI-led pipeline, despite macro headwinds and rising GenAI disruption concerns. Further, the ~2.5% QoQ depreciation in average INR against the USD is expected to provide a meaningful translation tailwind to reported INR revenues and margins. Supportive cross-currency movements should also add ~0% to 0.5% sequential uplift to USD revenues.

Against this backdrop, we expect sequential revenue growth in the range of ~0.5% to 9%+ in INR terms across the coverage universe. We have revised our Target Prices factoring in the revised USD/INR rates and any respective new developments including large deal wins and M&As.

AI-led Efficiencies to Support Margin Performance

Margins are expected to remain positively skewed, with select companies likely to deliver 0% to 1.9% sequential expansion, driven by productivity-led efficiencies and continued cost optimization initiatives. That said, the benefit may be partially offset by wage revisions, integration costs from acquisitions, and higher SG&A investments in select companies.

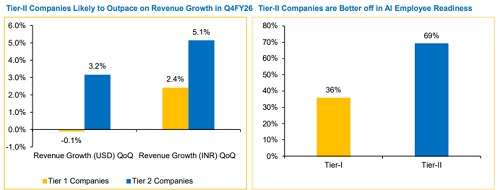

Mid-cap IT Still Best Placed for Relative Outperformance

As highlighted in our earlier note, we continue to prefer mid-cap IT, and believe this positioning remains well supported in Q4FY26. We expect mid-cap players to deliver better organic sequential performance than Tier-1 peers, driven by stronger demand traction, better execution resilience, and a more favorable growth profile. This relative strength is also likely to be supported by currency tailwinds, further reinforcing our constructive stance on the segment. Our preferred long-term investment ideas remain COFORGE, PSYS, HAPPSTMN, and FRACTAL.

Valuation and Preferred Ideas

* Tier-II Structural Beneficiaries of the Next Technology Cycle • Better Aligned to the Emerging Industry Model

* Valuations Have Turned More Supportive

Hence, our preferred long-term investment ideas remain; COFORGE (65% upside), PSYS (25% upside), HAPPSTMN (58% upside) and FRACTAL (24% upside).

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131