Indian Agrochemicals Industry: Slow Recovery With 6-8% Growth in FY27 by CareEdge Ratings

Synopsis

* The Indian agrochemicals industry (excluding fertilisers) is expected to witness stable growth of approximately 6-8% in FY27, supported by steady domestic demand, improving crop intensity, and expanding distribution reach. While global uncertainties persist, the industry is transitioning to a volume-led growth phase, with a gradual improvement in overall operating conditions.

* The sharp correction observed in FY24, driven by channel destocking and steep price declines, has largely played out, with inventory levels now largely normalised and volumes improving across key regions such as Latin America, North America, and parts of Asia. However, pricing remains competitive due to oversupply, particularly from China, which continues to dominate the supply of key intermediates and active ingredients.

* Geopolitical developments, particularly the ongoing US-Israel-Iran conflict, have introduced volatility in energylinked input costs and global logistics. While the temporary ceasefire has provided near-term stability by easing immediate pressure on crude oil prices and freight rates, the situation remains uncertain, with the risks of renewed disruptions.

* At the sectoral level, the performance of listed Indian agrochemical companies has improved, with revenues recovering on the back of volume growth. At the same time, profitability has strengthened, supported by cost normalisation and improved product mix. Operating margins, which had declined sharply in FY24, have recovered in FY25 and FY26, moving closer to levels observed during FY22–FY23.

Strong Domestic Demand with Stabilising Exports

The Indian agrochemicals sector continues to benefit from strong underlying agricultural fundamentals, with domestic demand providing a stable base for sustained growth. Despite global volatility, India remains a structurally growing market, supported by increasing agricultural activity and improving farm economics. Agrochemical demand in India continues to be supported by structural drivers. Cultivated area increased to about 29.5 million hectares in FY25 (PY: 29.1 million hectares). At the same time, foodgrain production rose to around 369 million tonnes (PY: 355 million tonnes), reflecting higher cropping intensity and a growing need for crop protection inputs. In addition, policy support and expansion in distribution networks remain key enablers, with the number of pesticide sale points increasing steadily to over 3 lakhs by FY25, thereby improving last-mile accessibility and supporting deeper market penetration

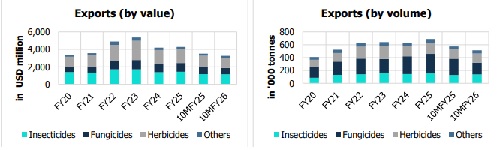

India continues to maintain a strong position in global agrochemical exports. Export volumes have expanded to nearly 0.7 million tonnes in FY25, reflecting sustained global reliance on Indian manufacturers. In FY26, export volumes stabilised, supported by steady demand in the United States and gradual recovery in select European and LATAM markets, even as some regions continued to adjust from previously elevated inventory levels. Entering FY27, export growth is expected to remain gradual and largely volume-led, supported by normalised channel inventories, stable global demand, and improving traction in key export regions. However, pricing pressures are likely to persist amid continued global oversupply. The export mix reflects a balance between scale and value. Fungicides contribute significantly to volumes, supporting capacity utilisation, while herbicides and insecticides generate relatively higher value per unit. This balanced product mix supports operating efficiency and earnings stability, particularly during periods of pricing pressure.

Stabilized Raw Material Pricing

The cost of key agrochemical inputs has largely stabilised at lower levels following the correction seen over the past two years. This stabilisation has improved cost visibility, enabling manufacturers to plan production more efficiently, optimise inventory levels, and streamline procurement strategies. While stable input costs support operational efficiency and margin management, they also intensify competition, particularly in commoditised products where pricing differentiation is limited. As a result, industry growth is increasingly volume-driven, with companies focusing on cost optimisation, product mix improvement, and operational discipline to sustain profitability in a competitive environment

Overall, the sector’s ability to balance scale-led volume growth with selective value accretion, while navigating stable but competitive input cost dynamics, remains central to maintain earnings resilience in a challenging pricing environment. Ongoing geopolitical conflict, if prolonged, could result in a significant increase in these key input costs.

Industry Performance Strengthened with Volume-Led Recovery

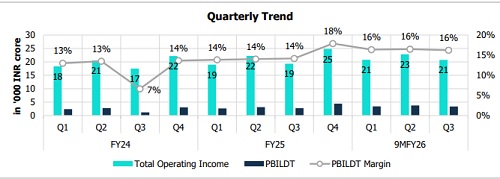

Following sharp inventory destocking and price correction in FY24, the industry witnessed a clear improvement in FY25, with total operating income of the top 24 listed players growing by approximately 9% year-on-year, supported by volume recovery, easing of channel destocking, and stabilisation in demand across key export markets. Operating performance strengthened in tandem, driven by lower raw material costs, improved capacity utilisation, better product mix, and operating leverage benefits.

Over the period from FY18 to FY25, the industry maintained a compounded annual growth rate (CAGR) of approximately 14.5% in total operating income, reflecting strong long-term growth despite cyclical fluctuations. This growth was supported by expansion in export markets, capacity additions by leading players, and increasing penetration of crop protection products across key agricultural regions. The growth trajectory, however, has been uneven. FY24 was characterised by a sharp correction, with revenues declining by approximately 14% year-onyear.

The chart above indicates a recovery phase beginning FY25, with TOI growth rebounding to around 9%, aided by steady export demand, gradual normalisation of channel inventories, and stabilisation in agrochemical raw material costs. This improving trend has continued till 9MFY26, with revenues remaining stable in the range of Rs 21,000- 23,000 crore and operating margins sustaining at around 16%, indicating improved earnings stability and operating discipline across the sector. The upward trajectory is expected to sustain into FY27, although growth is likely to remain volume-led rather than price-led, given ongoing competition and limited pricing headroom. Looking ahead, the industry is expected to grow by approximately 6-8% in FY27, largely driven by volumes, with margins gradually improving towards ~17%, supported by operating leverage and stable demand conditions. However, the operating environment remains exposed to external factors, particularly the US-Israel-Iran conflict, which has led to volatility in crude oil prices and logistics costs. While the temporary ceasefire has provided near-term stability, input cost trends remain a key monitorable, and margins would remain sensitive to evolving geopolitical developments.

Monsoon Remains Key Driver, Uneven Distribution a Risk

Rainfall remains a key determinant of agrochemical demand in India. Rainfall was good in the last couple of years, but looking ahead to FY27, the India Meteorological Department (IMD) has indicated a rainfall outlook of ~92% of the long-period average, due to the impact of El Niño, which could result in uneven rainfall across the country, potentially leading to region-specific demand variability and affecting overall agrochemical consumption.

Impact of Geopolitical Conflict and US Tariffs

The ongoing geopolitical conflict contributes to elevated macro and operating uncertainty for the agrochemical industry, primarily through energy prices, logistics costs, and currency volatility, rather than direct demand disruption. Agrochemical demand has remained largely resilient, given its linkage to food security and agricultural activity, although short-term ordering behaviour may remain cautious. Volatility in crude oil and freight markets poses margin sensitivity, especially for players with limited backward integration or greater reliance on imported intermediates. Supply chain disruptions, including longer transit times and higher insurance costs, will weigh on the profitability of Indian companies.

The USA remains a key market for Indian agrochemical exports, contributing approximately 20-30% of total pesticide exports. Q1 and Q2FY26 remained largely unaffected, as the additional 25% tariff was implemented only from August 2025. While export share moderated during September–October 2025 (~22-23%), exports rebounded in November 2025, indicating effective pricing adjustments and cost-sharing mechanisms, before stabilising at ~19- 23% in subsequent months.

Following the US Supreme Court ruling, tariffs have been reset to approximately 10%, materially easing earlier concerns around competitiveness and cost pass-through. As a result, the impact on volumes has remained limited, with adjustments largely reflected through pricing and margins rather than demand contraction. Going forward, while the lower tariff regime is supportive, margin sensitivity persists, necessitating continued focus on product mix optimisation and geographic diversification to mitigate concentration risk.

CareEdge Ratings’ View

The Indian agrochemicals industry has largely emerged from the sharp inventory-led correction in FY24 and is entering a phase of more stable, volume-driven growth, as seen in FY25 and 10MFY26. Normalisation of channel inventories across export markets, steady domestic demand supported by rising cropped area, improving irrigation coverage, low per-hectare chemical usage, and a stable input cost environment have improved earnings visibility across the sector. While pricing pressures are expected to persist amid elevated global supply and competitive intensity, particularly in generic molecules, operating performance has strengthened, aided by better capacity utilisation, cost normalisation, and selective product mix optimisation. However, margins remain sensitive to external factors such as energy prices and logistics costs, which are influenced by geopolitical developments.

“CareEdge Ratings expects the Indian agrochemicals industry to witness stable growth of around 6-8% in FY27, primarily driven by volume recovery, steady domestic demand, and improving export traction, even as pricing pressures persist in a competitive global environment. While operating performance has improved from FY24-FY25 levels, margin recovery is expected to be gradual and remains exposed to external factors, including input cost volatility, geopolitical developments, and supply chain disruptions. Companies with strong operational discipline and diversified exposure are likely to be better positioned,” said Arti Roy, Associate Director, CareEdge Ratings.

Above views are of the author and not of the website kindly read disclaimer