Research Report on Elder Care by CareEdge Ratings

Synopsis

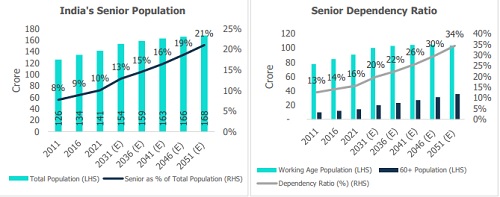

* India’s 60+ age population is projected to rise from ~142 million in 2021 to 231 million by 2036, taking its share in total population from ~10% to ~15%. The old-age dependency ratio is expected to rise from 15.7% in 2021 to 22.5% in 2036, signalling a meaningful structural shift in care needs and household support burden.

* India is ageing faster than its social-security architecture can absorb: 70% of elderly depend on family for daily maintenance, 78% lack pension cover, and inpatient out-of-pocket spend remains high. This makes eldercare not just a healthcare issue, but also a financing challenge.

* Healthcare demand intensity is likely to rise sharply as 75% of the elderly have at least one chronic disease and 1 in 4 faces multimorbidity, while India has only ~16 hospital beds per 10,000 people. To reach even ~25 beds per 10,000, India may need to add ~75,000 beds annually over the next 25 years with an annual investment of Rs 40,000-50,000 crore.

* At the same time, the ageing population creates a sizeable long-term opportunity for the silver economy, including hospitals, diagnostics, home healthcare, assisted living, senior housing, and other organised eldercare services. By 2036, the specialised senior care market could be ~USD 35 billion per annum.

India’s Demographic Transition: A Defining Structural Shift

Presently, India is among the youngest large countries, with an average age of just 29 years. However, India’s demographic profile is expected to undergo a massive transformation over the next two decades, leading to changes in economic and social structures. India’s senior/elder population (60+) is estimated to be ~142 million (10% of the total population) in 2021 and is expected to grow to ~231 million by 2036 (15% of the total population) and to ~340-350 million (~21% of the population) by 2051, growing at a CAGR of over 3%.

India’s total fertility rate (TFR) has been falling rapidly over the last few decades, and it is now at 1.9, below the replacement level of 2.1. At the same time, life expectancy has improved considerably. Both factors are expected to increase the senior/elder dependency ratio (senior population/working-age population) over the next two decades. A study published in The Lancet in March 2024 indicated that TFR can fall to as low as 1.3, leading to an even greater demographic shift than currently projected.

Compared to developed economies such as the USA, UK, and Japan, where ageing trends are more gradual and partly offset by immigration, India’s demographic shift will occur at a significantly higher scale and speed, posing unique economic and social challenges.

Emerging Healthcare Challenges

1. Healthcare Financing Gap

Spending on healthcare grows rapidly with the progression of age. India’s cultural trend is to rely on children for financial support in retirement. However, the increasing prevalence towards nuclear families and migration leaves elders without support. The increasing dependency ratio (from 15.7% in 2021 to 22.5% in 2036) places a greater burden on the working-age population. As per NITI Aayog’s position paper ‘Senior care reforms in India – reimaging the senior care paradigm’, 70% elderly are dependent on family for everyday maintenance, and 78% of elders are without pension cover. Over 80% of Indians today work in the unorganised sector, without any pension support or sizable retirement savings. The Government of India (GOI) has tried to address this challenge via several schemes such as Old Age Pension Schemes, Atal Pension Yojana, Varishtha Pension Bima Yojana, Pradhan Mantri Vaya Vandana Yojana, etc. However, enrolment and pension entitlement remain inadequate. Around 86% of the enrolees in the Atal Pension Yojana have opted for the lowest possible pension slab of Rs.1,000 (Source: Press Information Bureau, GOI). At the same time, the mean out-of-pocket expenses (OOPE) for elderly patients in inpatient care are ~Rs 8,000 in public facilities and ~Rs 31,933 in private facilities.

Significant efforts have been made to expand health insurance coverage. As per the last Longitudinal Ageing Study in India (LSAI) commissioned by the Ministry of Health and Family Welfare, only 18% of people aged 60 and above were covered by health insurance. However, the introduction of Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (PMJAY) widened the insurance net. In September 2024, the Government of India decided to expand the insurance net under PMJAY further, covering all citizens aged 70 years and above. According to CareEdge Ratings’ estimates, over 50% of India’s population is expected to be under health insurance coverage over the next 3-4 year

PMJAY and private insurers mostly cover inpatient expenditure, leaving the elderly with significant exposure to OOPE for routine check-ups, medicines and treatments. Further, the requirement of a caregiver in case of disability or impairment increases the burden on the family in the absence of an assured pension or insurance reimbursements.

In developed regions, demographic transition has unfolded gradually over a longer period; these countries have had more time to adapt to the rising share of older adults. As a result, they have established stronger healthcare systems and consistently invested more per capita, allowing their service models to evolve and mature over time.

2. Healthcare Infrastructure Gap

For several decades, healthcare policies and programs in India have largely focused on priorities such as disease prevention and control, maternal and child health, and population stabilisation. In contrast, areas like long-term palliative care and elder care have remained relatively underemphasized. As per LSAI, 75% of the elderly have one or more chronic diseases, and 1 in 4 has multiple morbidities. Seniors have more hospitalisation needs. With a change in the demographic profile, India’s disease burden is also expected to change to degenerative and noncommunicable diseases (NCD).

Demographic change will put additional pressure on the already strained healthcare infrastructure. China’s elder population (as % of total population) today is similar to what India’s will be in 2050 (Source: UN World Population Prospects 2024). According to the WHO, China has over 55 hospital beds per 10,000 people, compared to ~16 in India. To reach at least ~25 hospital beds per 10,000 people, India will have to add at least 75,000 hospital beds per annum over the next 25 years, requiring an annual capex of at least ~Rs 40,000-50,000 crore (excluding inflation) to build hospital infrastructure. The private sector can add only 7,000 to 8,000 beds per annum, and budget allocations from the state and central governments for creating hospital infrastructure remain highly deficient.

A gap also exists in the availability of human capital for the elderly’s needs. Shortage of doctors and skilled nursing personnel is well known, especially in rural areas. Due to the increasing prevalence of nuclear families, migration and declining TFR, an increasing number of elders will need home care, specialised senior living, assisted living, and full-time nursing care. Failure to adequately train the workforce will lead to an acute shortage of skilled people amid rising demand. Keeping this need in mind and existing opportunities for medical tourism, the Union budget 2026-2027 has planned to train 1,00,000 allied professionals over the next 5 years. Union budget 2026-2027 has also introduced a major caregiver programme to train over 1.5 lakh multi-skilled caregivers. Given that 7 out of 10 elderly people reside in rural areas, the availability of a skilled workforce there will help improve overall eldercare outcomes.

Specialised Senior Care: A Multi-Decade Opportunity

Despite structural challenges, India’s ageing population presents a substantial economic opportunity—often referred to as the “silver economy.” Future elderly cohorts are expected to be relatively more financially secure. A steady increase in the serviceable population (>3% CAGR) and significantly higher disposable income/wealth (compared to what was available with earlier and present seniors) of that serviceable population, could create a multiplier effect for India’s silver economy. Apart from hospitals and pharmaceuticals, associated services such as preventive diagnostics, health supplements, personalised medication, home care, and assisted living could also see sizable growth in their respective market size.

Opportunities also exist for specialised senior living facilities. Penetration of specialised senior living facilities is less than 0.5% in India compared to ~6% to 7% in the USA and ~7% to 10% in China. Assuming 3% penetration over the next 10 years and spend of ~Rs 40,000 per senior per month by 2036, the specialised senior care market could be ~USD 35 billion per annum. Presently, the southern Indian states lead the specialised senior living market on account of a higher senior population (as a % of the total state population) and higher per capita income.

Several Indian and global corporates are engaged in developing specialised senior home and assisted living facilities. Ashiana Housing Limited, Max Estates Limited via its brand “Antara Senior Living”, Columbia Pacific via its brand “Serene Communities”, Athulya Senior Care, Covai Care, Vedaanta Senior Living, etc.

Conclusion

India stands at the cusp of a major demographic inflection point. The transition from young to an ageing population will reshape the country’s economic structure, healthcare demand, and social fabric. While the challenges, particularly around financing, infrastructure, and workforce, are significant, they also create a compelling opportunity for policymakers, healthcare providers, and private sector participants to innovate and scale solutions. A coordinated approach involving policy support, private investment, and technological integration will be critical to ensuring that India can effectively manage this transition while unlocking the full potential of its emerging silver economy.

"India’s demographic transition is not just a social shift but a structural economic change. The rapid rise in the elderly population, coupled with evolving family dynamics and limited pension coverage, will significantly increase demand for organised eldercare services. This creates a long-term opportunity for healthcare providers, insurers, and senior living operators to build scalable and sustainable solutions", said Krunal Modi, Director, CareEdge Ratings.

“While the opportunity in the silver economy is substantial, bridging the gaps in healthcare infrastructure, insurance coverage, and skilled workforce will be critical. The sector will require sustained investments and policy support to ensure accessibility and affordability, especially in non-urban regions where most of the elderly population resides”, said Dhruv Shah, Assistant Director, CareEdge Ratings.

Above views are of the author and not of the website kindly read disclaimer