GLP of Microfinance Industry Expected to Reach ~Rs 5.5 trillion By -CareEdge Ratings

Synopsis

• NBFC MFIs Gross Loan Portfolio (GLP) is expected to have crossed Rs 3.3 trillion in FY26, driven by improving demand in rural and semi-urban markets and stronger underwriting practices. While the near-term outlook

remains cautious as institutions stabilise asset quality and borrower leverage levels, the ongoing correction is expected to strengthen underwriting discipline and support sustainable long-term growth.

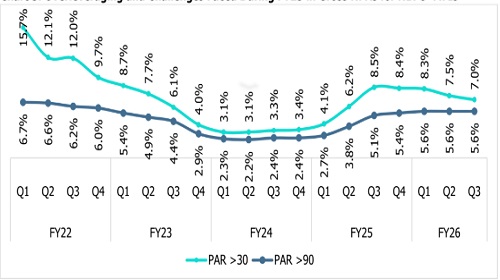

• After a period of strong growth until FY24, the sector entered a corrective phase driven by asset quality deterioration, borrower overleveraging and regulatory tightening. Portfolio stress remained elevated in Q3FY26,

with PAR>30 and PAR>90 at 7.0% and 5.6%, respectively, while NPAs may witness a marginal increase in FY27 as institutions normalise their write-off practices.

• Following a strong recovery in FY23 and peak profitability in FY24, the industry’s profitability declined sharply, with Pre-Tax RoA at around -1.7% in FY25 due to elevated credit costs. Profitability is estimated to have improved

to -0.1% in FY26, supported by stabilising asset quality, moderating credit costs and strengthened underwriting standards.

• Microfinance Industry Network (MFIN) introduced additional guardrails, including borrower indebtedness caps and stricter delinquency norms, to strengthen responsible lending and improve long-term sustainability.

Landscape of Indian Micro Finance Industry (MFI)

MFI primarily caters to low-income households and women borrowers, bridging the gap between formal credit and underserved communities through small-ticket loans that support livelihoods and entrepreneurship. The industry has evolved from a niche lending segment into a significant component of the country’s financial ecosystem, supported by regulatory reforms, institutional consolidation, improving access to funding and increasing digitisation. NBFC-MFIs continue to play a crucial role in extending formal credit access to financially excluded populations, particularly in rural and semi-urban regions.

While the industry continues to face challenges such as elevated funding costs, regional concentration risks, borrower overleveraging and asset quality pressures, its resilience and adaptability have enabled it to remain a

key driver of financial inclusion in India. The sector continues to contribute significantly to women's empowerment, rural economic development, and the expansion of formal financial services across underserved

communities.

Note: P – Projected; Data includes data for Banks JLG, SFBs, NBFC-MFIs, other NBFCs and non-profit MFIs.

Source: MFIN, CareEdge Advisory

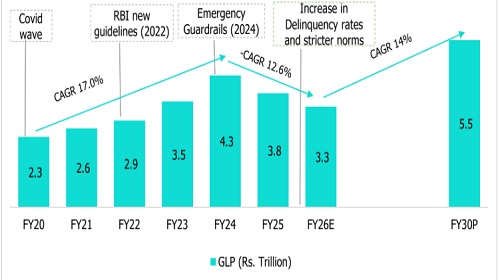

CareEdge Advisory observes that MFIs are now beginning to experience favourable sectoral tailwinds. Their

performance in terms of portfolio growth has improved, with GLP expanding from Rs 2.3 trillion in FY20 to an

estimated Rs 3.3 trillion in FY26. However, it remains moderate due to persistent stress in certain impacted

segments of the portfolio. Following the pandemic-led disruptions, the industry experienced a strong rebound in

FY23 and FY24, supported by pent-up credit demand, improving economic activity and accelerated adoption of

digital lending platforms, resulting in GLP peaking at Rs 4.3 trillion in FY24.

However, the rapid growth phase also led to challenges such as borrower overleveraging, elevated field staff

attrition, and weakening asset quality across certain regions, leading the sector into a corrective phase.

Consequently, GLP declined by 13.5% Y-o-Y to Rs 3.8 trillion in FY25 and is further estimated to have moderated

to Rs 3.3 trillion in FY26. The moderation was largely systemic and prompted lenders to tighten underwriting

standards and prioritise portfolio quality over aggressive growth. While the near-term outlook remains cautious as

institutions stabilise asset quality and borrower leverage levels, the ongoing correction is expected to strengthen

underwriting discipline and support sustainable long-term growth. Accordingly, the MFI’s GLP is projected to recover

and grow at a CAGR of 14% during FY26–FY30P, supported by improving operating conditions, increasing formal

credit penetration and sustained demand for financial inclusion.

The projected recovery reflects expectations of gradual improvements in collection efficiency and lender confidence,

as well as growth in both borrower base and average ticket sizes. Historically, the sector has demonstrated strong

rebounds following periods of disruption.

However, unlike previous cycles, the current regulatory framework incorporates tighter controls on borrower

leverage, bureau monitoring and multiple-lending practices. As a result, projected growth is expected to be driven

largely by deeper penetration among underserved borrowers and disciplined credit underwriting, rather than

borrower overlap and rapid portfolio expansion.

Note: P – Projected; Data includes NBFC MFI, players.

Source: MFIN, CareEdge Research

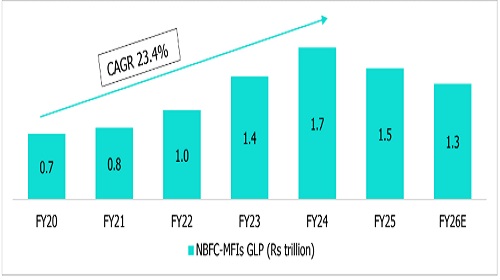

The NBFC-MFI industry remained resilient over the past few years, with GLP increasing from Rs 0.7 trillion in FY20

to an estimated Rs 1.3 trillion in FY26 despite challenges such as the pandemic, inflation, higher funding costs and

tighter regulations.

The sector witnessed strong growth in FY23 and FY24, supported by rising credit demand, economic recovery and

digital lending adoption, with GLP peaking at Rs 1.7 trillion in FY24. However, GLP moderated to Rs 1.3 trillion in

FY26, down nearly 23.7% from the FY24 peak, as lenders tightened underwriting standards and prioritised portfolio

quality. Rapid post-COVID expansion led to borrower overleveraging and asset quality pressures, resulting in a

corrective phase. The ongoing correction is expected to support more sustainable long-term growth for the sector.

Asset Quality for NBFC-MFIs

MFIN introduced guardrails to promote responsible lending practices further and strengthen borrower protection,

which include mandatory e-validation of Voter ID, restricting borrowers to a maximum of three microfinance

lenders, capping total microfinance indebtedness at Rs. 2 lakhs, and tightening delinquency norms by restricting

lending to borrowers with DPD > 60 days (previously 90 days) on loans exceeding Rs 3,000 with any regulated

entity.

Following the guardrails, PAR>30 remained elevated at 7% in Q3FY26, and PAR>90 stood at 5.6%, indicating that

incremental stress is flowing into higher delinquency buckets. The sustained elevation in PAR>90 suggests that

asset quality pressures are not transitory and may keep credit costs elevated in the near term.

Above views are of the author and not of the website kindly read disclaimer