India Strategy : Macro uncertainties mount; Midcaps sustain outperformance by Motilal Oswal Financial Services Ltd

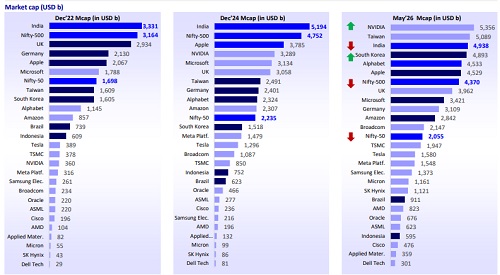

‘Big Tech’ market cap surge dwarfs that of India and other key EMs

* The AI-led rally has reshaped global market rankings. In USD terms, India’s market capitalization now trails NVIDIA and Taiwan, despite ranking well ahead of them only a few years ago.

* The Nifty-500’s market capitalization is now smaller than Taiwan, South Korea, NVIDIA, Alphabet, and Apple, reflecting the extraordinary scale of the AI and Big Tech boom. Capital, earnings, and investor flows are becoming increasingly concentrated in a handful of technology leaders, raising concentration risks even as the AI theme continues to drive global market performance

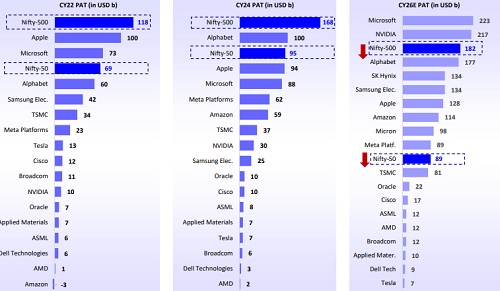

* Expanding earnings delivery and rising expectations are also propelling Big Tech higher in the earnings rankings.

* Earnings for most of the major tech names have risen notably. Microsoft & NVIDIA’s earnings are now likely to surpass the agg. Nifty-500 earnings in 2026E.

* Further, eight Big Tech names have climbed the earnings ranks, surpassing the Nifty-50 over the past two years.

* Therefore, no wonder capital is chasing the expanding earnings growth in AI and Big Tech plays

More legs to the ongoing AI rally: Strong earnings growth trajectory continues

Strong earnings visibility and supportive valuations

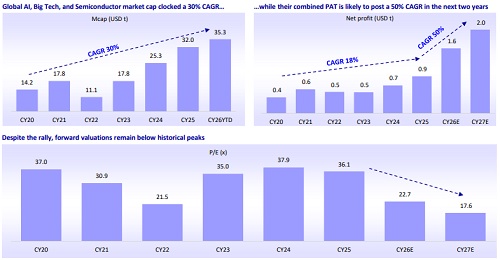

* While CY24 and CY25 were the years of a global AI and semiconductor boom, with market cap and profits recording ~34% and ~32% CAGR, respectively, valuations have stretched to multi-year highs. However, this does not appear to ring alarm bells given the strong earnings trajectory of global AI and chip/ semiconductor manufacturing companies.

* Earnings are expected to clock ~46% CAGR over the next two years, underscoring the durability of the underlying growth cycle.

* While multiple pockets within the category do appear stretched, overall, valuations look moderate on a forward basis, nearly half of the current levels

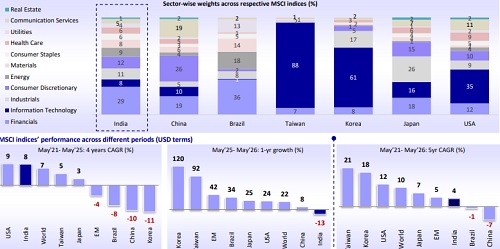

India’s market remains the most diversified across sectors among EMs

* India has recently witnessed FII outflows amid concerns over a lack of material AI-linked opportunities, while AI-heavy markets such as Taiwan and Korea have attracted strong inflows driven by AI-related trades. This divergence largely reflects the sectoral composition of major equity markets, where technology dominates Taiwan, Korea, and the US, while financials remain the largest sector in India, China, and Brazil.

* The top 3 sectors account for nearly 96% of the MSCI Taiwan Index, 86% in Korea, 68% in Brazil, 64% in China, 60% in Japan, and 58% in the US, compared with only ~52% in India. This highlights India’s relatively diversified market structure with broader sector representation and lower concentration risk.

* MSCI India severely underperformed other key markets in the past one year while it significantly outperformed them before the start of the AI rally. Any reversal or moderation in AI-led trade could significantly benefit the diversified markets such as India, while disproportionately impacting the technology-heavy markets that remain more dependent on AI-driven flows and sector concentration.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Nifty immediate support is at 25000 then 24800 zones while resistance at 25222 then 25350 z...