Hold L&T Technology Services Ltd For Target Rs.3,610 by Prabhudas Liladhar Capital Ltd

Cleanup completes, Execution now key for recovery

Quick Pointers

* Restructuring & portfolio rationalization completes in Q4

* TCV wins of US$ 855 mn in FY26

LTTS reported a subdued Q4, impacted by portfolio restructuring, including divestment of its SWC business (primarily India-focused smart cities) and the exit of ~US$19 mn annualized low-margin, non-strategic engagements across geos. These actions, part of its 5-year Lakshya program (targeting 13–15% USD revenue CAGR and 16–17% EBIT margins), are now largely complete. With the portfolio reset behind it, LTTS expects a return to broad-based growth from Q1FY27, led by a recovery in Tech as restructuring-related drag abates, sustained strength in Sustainability, and an improving outlook in Mobility supported by recovery in auto and strong deal wins. Deal momentum remained robust with FY26 large deal wins at US$855mn (+40% YoY), providing revenue visibility as these ramp up; however, we expect the near-term recovery to be gradual as the company works to offset the revenue impact of exited businesses. We therefore model FY27E USD revenue growth at 5.4% (vs. 8.3% growth in FY26 continuing business), while largely retaining our FY28E growth estimates. On margins, restructuring benefits are already visible, and shift toward higher-margin segments should drive further expansion. Management now targets achieving mid-16% EBIT margins earlier than its prior Q4FY27 timeline; we factor this in by raising our FY27E EBIT margin estimate to 15.3% (from 15.0%), while maintaining FY28E margins at 15.5%. We assign PE of 23x (earlier 24x) to FY28E EPS to arrive at TP of INR 3,610 and downgrade our rating to HOLD (earlier BUY)

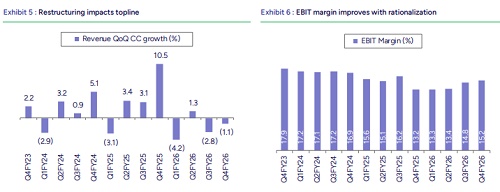

Revenue: LTTS in Q4 reported Q4 revenue of US$306mn, down 1.1% QoQ CC in the continuing business. Segment-wise, Sustainability grew 1.6% QoQ, while Mobility and Tech declined 0.4% and 6.3% QoQ, respectively. For FY26, LTTS reported revenue of US$1.23bn, up 7.7% YoY CC in continuing operations, while including discontinued business, revenue stood at US$1.32bn, reflecting 4.7% YoY CC growth.

Operating Margin: LTTS reported Q4 EBIT margin of 15.2%, up 40 bps QoQ above our and consensus estimates of 14.4%, driven largely by gross margin expansion supported by an improved revenue mix. Segment-wise, Mobility and Tech margins improved by 170 bps and 190 bps QoQ, respectively. For FY26, LTTS reported an EBIT margin of 14.5%, down 90 bps YoY.

Deal Wins: Q4 deal wins remained strong, with large deal TCV of US$ 182mn in Q4, largely driven by wins in higher-margin segments of Mobility and Sustainability. For FY26, LTTS secured large deal TCV of US$ 855mn (+40% YoY), positioning the company well for growth in FY27E.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271