FUND FOLIO (June 2026): Net equity inflows ebb in May`26 to a 12-month low by Motilal Oswal Financial services Ltd

SUMMARY: Net equity inflows ebb in May’26 to a 12-month low

Key observations

* The Nifty consolidated (down 1.9% MoM) in May’26 after rebounding smartly in Apr’26 with a 7.5% MoM gain. Notably, the index remained volatile and hovered around 1,220 points before closing 450 points lower. Notably, the Nifty Midcap 100 and Nifty Smallcap 100 outperformed the Nifty 50 and were up 3.2% and 0.7%, respectively. FIIs recorded outflows for the third consecutive month in May’26 at USD4.9b. In contrast, DII inflows remained strong at USD8.7b.

* Total AUM of the MF industry dipped marginally by 0.4% MoM to INR81.6t in May’26, primarily led by a MoM decrease in AUM of liquid (-INR506b), income (-INR376b), other ETFs (-INR48b), and gilt (-INR18b) funds. Conversely, AUM of equity increased INR407b, arbitrage funds rose INR84b, and gold ETF funds grew INR65b MoM.

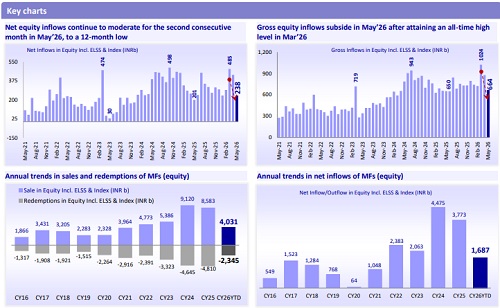

* Equity AUM of domestic MFs (including ELSS and index funds) rose 1% MoM to INR39.5t in May’26 despite bleak market sentiments. Redemptions declined 4.9% MoM to INR425b. However, an even higher fall in equity scheme sales (-24.4% MoM to INR664b) led to a decline in net inflows (to a 12- month low) to reach INR238b in May’26 from INR431b in Apr’26.

* Investors continued to park their money in mutual funds. Inflows and contributions in systematic investment plans (SIPs) stood at INR309.5b in May’26 (down 0.5% MoM and up 16% YoY).

A few interesting facts

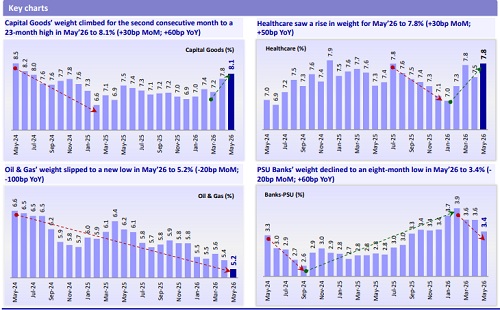

* The month witnessed notable changes in the sector and stock allocation of funds. On a MoM basis, the weights of Capital Goods, Healthcare, Automobiles, E-Commerce, NBFC – Non-Lending, and Cement increased, while those of Oil & Gas, PSU Banks, Technology, Consumer, Metals, Retail, and Real Estate moderated.

* Capital Goods’ weight climbed for the second consecutive month to a 23-month high in May’26 to 8.1% (+30bp MoM; +60bp YoY).

* Healthcare saw a rise in weight for May’26 to 7.8% (+30bp MoM; +50bp YoY).

* Oil & Gas’ weight slipped to a new low in May’26 to 5.2% (-20bp MoM; -100bp YoY).

* PSU Banks’ weight declined to an eight-month low in May’26 to 3.4% (-20bp MoM; +60bp YoY).

* The top sectors where MF ownership vs. the BSE 200 was at least 1% higher were NBFC – Non-Lending (16 funds over-owned), Healthcare (14 funds over-owned), Consumer Durables (11 funds over-owned), Chemicals (9 funds over-owned), and Capital Goods (8 funds over-owned).

* The top sectors where MF ownership vs. the BSE 200 was at least 1% lower were Oil & Gas (19 funds under-owned), Private Banks (15 funds underowned), Consumer (15 funds under-owned), PSU Banks (14 funds under-owned), and Utilities (12 funds under-owned).

* In terms of value change MoM, divergent interests visible within sectors: The top 10 stocks that witnessed the maximum rise in value were ICICI Bank, Adani Enterprises, Gujarat Gas, Samvardhana Motherson, Eternal, Lenskart Solutions, Solar Industries, Axis Bank, JSW Energy, and Adani Energy Solutions. Conversely, the stocks that witnessed the maximum MoM decline in value were SBI, Reliance Industries, ITC, Bharti Airtel, Infosys, TCS, HDFC Bank, ONGC, Torrent Power, and Power Grid.

Key trends: Gross inflows subside in May’26 after attaining an all-time high level in Mar’26

Weight allocation: Capital Goods and Healthcare gain, while Oil & Gas and PSU Banks slip

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

More News

SUMMARY: Equity inflows witness a slowdown; Automobiles hog the limelight by Motilal Oswal F...