Economics - India turning adversities to advantage in trade by Elara Capital

Amidst record depreciation of the USDINR, its benefits were witnessed in pushing up the level of both goods and services exports, although FX weakness coupled with elevated energy prices kept import bill elevated. Per latest data, India now exports more to other countries than to the US compared with pre-tariff period (Jan-25). On the oil imports side, geographical diversification was visible as the importance of Russia and Oman increased in India’s import basket (percentage share), while the share of Saudia Arabia and UAE declined on Y-o-Y basis in May-26.

Current account in surplus in April 2026:

The RBI’s monthly BOP release showed balance of payments deficit of USD6.6 bn in April, driven by FPI outflows of USD 8.7 bn and USD3.3 bn outflow under banking capital even as net FDI inflows rose to USD7.4 bn. The capital account remained a drag on the BOP as the current account recorded a surplus of USD 4.7 bn, led by remittances of USD16 bn and services surplus of USD18.6 bn.

Weaker Rupee helping India’s goods trade:

India’s overall exports rose by ~16% YoY to USD ~82bn with goods exports rising by 18% YoY to USD 45.2bn – the highest on record. On the other hand, imports rose by 20.6% YoY to USD 73.4bn, leading to widening of goods trade deficit to USD 28.2bn from USD 22.6bn in May-25. Per our estimates, the FX adjusted exports were USD 34.2bn and imports USD 54.4bn, leading to a trade deficit of USD 20.2bn.

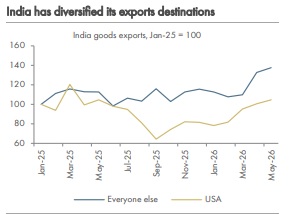

India successfully diversified export destinations:

In May India’s goods exports to other countries, excluding the USA, were up by 37% vs pre-tariff period (Jan-25=100) vs. 4% growth in exports to the US. Note that India’s exports to the US are down 13% in May-26 from Mar-25 peak of USD 10.1bn when US importers were advancing purchases before The Liberation Day tariffs.

On the import side, the key signal is in the sourcing geography:

The top import sources exhibiting the highest value growth in May 2026 relative to May 2025 were Oman (+306% YoY), Russia (+63.46%), the US (+54.43%), and China (+23.4%). The rise for Oman and Russia reflects diversification of source of oil imports. Imports from Oman at ~USD 2bn, were highest in a decade. Imports from Taiwan and China have risen to near record (Taiwan) and record highs (China), possibly underpinned by electronics imports and surging semiconductor/RAM prices

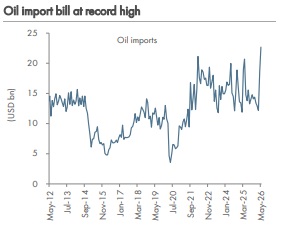

Oil price impacted overall goods trade deficit:

Elevated crude oil and derivatives prices due to the Middle East conflict impacted the overall import bill. Oil imports were at record USD 22.7bn in May-26 and the net oil import bill rose to USD 14.3bn, near record highs. Crude prices accelerated exports too, but the quantum was lower at USD 8.4bn, higher than May25 levels of USD 5.4bn but lower than Apr-26 exports of USD 9.6bn.

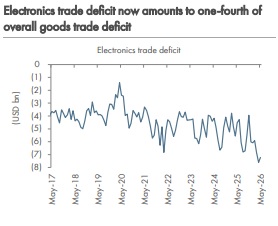

Electronics trade deficit now forms one-fourth of India’s goods trade deficit:

The rising influence of electronics is becoming clearer, as electronics trade deficit rose to USD 7.2bn in May-26 vs. USD 4.5bn in May-25. At 7.2bn, it is 25% of India’s goods trade deficit. Expected positive tailwinds from weaker INR are yet to be visible in electronics exports as over last six months, electronics imports rose by 26.3% YoY on an average, while exports rose less nearly half the pace of imports at an average of ~13% amid weak mobile demand globally.

Outlook – India’s export outlook is challenging for FY27, but worst is over:

In the upcoming months, softness in crude oil prices, and potential moderation in freight costs due to opening of the Strait of Hormuz can normalize the import bill towards the run rate of USD 60bn per month. Exports growth may be capped in the short run due to moderating global demand and crude oil availability to export crude products. However, gains of 10% INR depreciation (vs last year) and continued strength in services exports and remittances are likely to cap the drag on Current Account. Important to monitor hereon is also the passthrough of elevated producer prices in China amidst strengthening RMB. India runs an annual trade deficit of USD 112bn with China. Add to this, surging electronics costs may keep electronics import bill (17% of total imports) elevated.

Above views are of the author and not of the website kindly read disclaimer

.jpg)

.jpg)