Diet Report - Utilities - BESS tendering activity in full swing by Elara Securities

BESS tendering activity in full swing

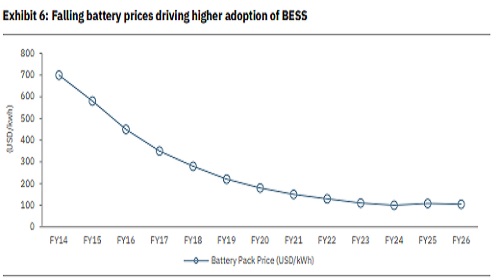

Renewables tendering activity slowed sharply in solar and wind while battery energy storage systems (BESS) bucked the trend. In FY26 YTD, solar tenders fell 28% YoY to 23.5GW and wind declined 49% YoY to 2.8GW, with Firm and dispatchable tenders (FDRE) down 28% YoY to ~9.2GW amid a ~43GW power purchase agreement (PPA) backlog, deferred State procurement, tariff expectations, and transmission concerns; awards mirrored this weakness, with solar down 74% YoY to 3.1GW, wind down 55% YoY to 900MW, and FDRE slipping 6% YoY to 7.1GW. In contrast, BESS gained strong traction, with 32.7GWh of tenders floated vs 15GWh YoY and 16.0GWh awarded vs 3.5GWh YoY, led by ~30% VGF support, ~40% lower tariffs for VGF-backed projects, and an 8% decline in average battery prices in CY25, with BESS cost nearly one-third of CY20 levels, due to manufacturing gains, improved chemistry, and low Lithium Iron Phosphate (LFP) prices

Momentum fades in solar and wind tenders: A total of 23.5GW of vanilla solar tenders have been floated in FY26 YTD, marking a 28% YoY decline vs the same period in FY25. Wind tendering activity has been even weaker, falling 49% YoY to 2.8GW. Similarly, firm and dispatchable renewable energy (RE) tenders have dropped 28% YoY to ~9.2GW, indicating an overall slowdown in bidding activity across segments. The slowdown in tendering is due to a ~43GW backlog of renewable projects awaiting PPA signings. State utilities have deferred procurement, anticipated lower tariffs, and raising concerns over supply reliability amid transmission delays.

Awards activity slows in solar and wind: Mirroring the slowdown in tendering, awarding activity too has slowed in FY26 YTD. Awarding in the solar segment plunged 74% YoY to 3.1GW. Awarding in the wind segment fell 55% YoY to 900MW. Around 7.1GW of FDRE projects were awarded in FY26 YTD, down by 6% YoY.

BESS tenders defy sector slowdown: BESS continues to lead growth within the renewables segment. In FY26 YTD, 32.7GWh of battery storage tenders were floated — more than double 15GWh issued during the same period in FY25 — while awards rose sharply to 16.0GWh from 3.5GWh in the past year. This acceleration has been driven by the viability gap funding (VGF) scheme, which provides up to 30% capital support for standalone BESS projects, significantly improving project economics. VGF-backed tenders have delivered tariffs ~40% lower than non-VGF projects for two-hour storage solutions. Recent auctions in Andhra Pradesh (1,000MW, November 2025) and Gujarat (2,000MW, November 2025) discovered monthly tariffs as low as INR 189,000–150,000 per MW. The strong pipeline is further supported by declining battery cost —average prices fell 8% in CY25, due to manufacturing efficiency, advancement in battery chemistry, rising global competition, and ample supply. BESS prices recorded the sharpest drop, with global average in CY25 at nearly one-third of CY20 levels, aided by record-low lithium iron phosphate (LFP) battery prices. Rising peak electricity demand in India has significantly bolstered the popularity of solar and battery storage tenders. With peak loads reaching record levels in recent years, utilities and distribution companies (DISCOM) are increasingly seeking flexible and reliable solutions to manage supply during high demand periods. Solar projects, coupled with BESS offer a cost-effective way to meet these peaks.

Above views are of the author and not of the website kindly read disclaimer