Consumer Goods Sector Update : FMCG Review: Pace of acceleration in volume growth will be key By JM Financial Services

For our Staples (ex-ITC/VBL) coverage universe, 2QFY26 sales growth (+7% YoY) was in line while EBITDA (+2.5% YoY) was a tad better vs. our estimate, despite GST transition-led operational challenges, which had an impact of c.2-4% on sales growth. Key highlights were: a) F&B players (Nestle,TCPL,Britannia) positively surprised and outperformed HPC players (in-line quarter) and b) Commentaries point to uptick in volume growth across companies – benefit of festive period, GST transition-led MRP cuts/grammage increases (Britannia, Bikaji), and likely intense winter (Dabur, HUL). Britannia, Bikaji, Honasa, Marico and Honasa were quite upbeat about 2H outlook both on sales and EBIDTA margin. This is also visible from our and Street estimates for 2H (building uptick in sales and much higher growth in EBITDA vs. 1HFY26 trajectory). Sector valuation (NTM PE of c.55x) is above the 10-year average, thereby limiting headroom for error. Prefer Britannia, Marico, Dabur, Honasa and Bikaji within our coverage.

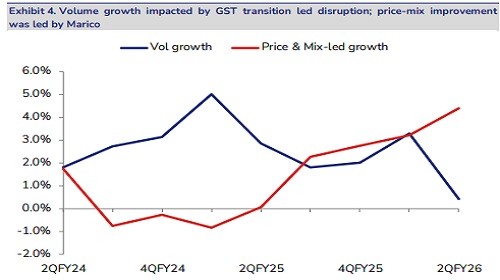

* GST transition impacts volume growth; EBITDA growth a tad better than forecasts: While price/mix growth saw some uptick (led by Marico), volume growth for most companies in our staples coverage universe (barring Dabur/Nestle) witnessed temporary moderation vs. 1Q – a function of GST transition led channel disruption (impact of 2-4% on sales). This impact is transient in nature and should normalise in 3QFY26E itself. Consumption of high cost inventory resulted in YoY compression in GM, although the extent of compression was lower vs. 1Q and QoQ margins improved across players barring Marico. A&P spends remained firm while overhead costs were tightly controlled, resulting in better-than-envisaged EBITDA growth.

* F&B players surprised positively and outperformed HPC players: Within staples, F&B players outperformed HPC players on both top line and profitability. Within our coverage universe, F&B sales/EBITDA grew by 8.1%/7.4% vs. 4.9%/-1.8% for HPC. If we double click further, within F&B - TCPL, Nestle, and Britannia surprised positively while VBL’s performance was relatively soft within the pack. The performance of HPC players was largely in line with our forecasts with Colgate and Jyothy Labs being key underperformers.

* Operating environment remains a mixed bag; management commentaries point to improving outlook: Management commentaries pointed towards urban consumption picking up while rural remains stable. While some GST transition-led impact was seen in October too, volume trend is expected to improve vs. 1H, led by festive demand, grammage increases and normalisation of trade channel operation. Premiumisation trend remains intact as seen in case of Marico (recovery in VAHO), HUL (B&W, premium hair care/soaps), Nestle (uptrading seen in coffee) and GCPL (LV, liquid detergents). Competitive activity remains firm – some HPC categories (Oral care/dishwash/soaps) saw higher promotional intensity while categories such as biscuits witnessed influx of new regional/local competition post GST transition.

* What has Street done to its estimates? With improving macros, festive/wedding season-led benefit and favourable base, Street expects recovery in performance both in sales and profitability in 2HFY26E vs. 1HFY26. Consensus estimates for FY26E suggests that the Street is factoring in high-single-digit revenue growth for 2HFY26E for staples coverage (exITC/VBL) led by uptick in volume growth (mid to high single-digit growth) and low double digit EBITDA growth.

* How do we see 2H shaping up? For 2HFY26E, we expect Marico to sustain its c.20%+ growth trajectory, followed by c.9-14% sales growth for key F&B players (Bikaji, Britannia, TCPL, Dabur and Nestle). We bake in 13% growth for Honasa, followed by c.10% growth for GCPL, while sales growth could be relatively lower at 5-7% for HUL, Colgate and Jyothy Labs. On the margin front, we expect healthy recovery despite stable-to-higher brand investments – a function of easing/stable RM prices and scale leverage. For coverage universe (ex-ITC/VBL), we expect c.10% YoY sales/EBITDA growth in 2H (vs. 7%/flat sales/EBITDA growth in 1H)

* Acceleration in sales growth will be key given limited headroom for error: Post the recent GST announcement, staples (ex-ITC) saw a brief rally in Aug’25 (traded above 5-year average); however, the same was largely offset as pre-quarter updates pointed towards transitory channel disruptions. With NTM PE at c.55x (higher vs. 10-year average though below 5-year average) and optimism built in street estimates, headroom for error is limited. Hence, pace of acceleration in volume growth will be key monitorable for rerating from current levels.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361

Tag News

Buy Honasa Consumer Ltd for the Target Rs 500 by Emkay Global Financial Services Ltd