Chana Report As On 20th June 2026 by Kedia Advisory

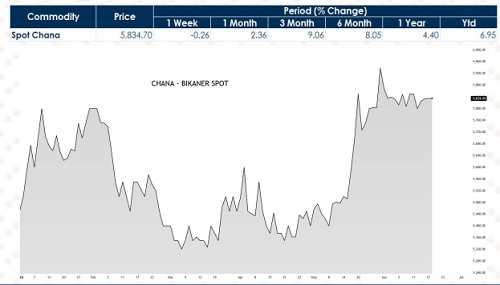

Price Performance: Chana prices gained nearly 2% on monthly basis as arrivals sharply declined across major mandis during May 2026. Arrivals for May 01–14 were reported at 1,25,223 tonnes, down more than 52% compared to 2,63,825 tonnes recorded during April 01–14. Lower arrivals and depleting old stocks supported sentiment, although easing gram WPI inflation by 7.71% year-on-year limited aggressive upside momentum.

Export Demand & Lower Imports Supporting Prices: Export demand remained a major supportive factor for chana prices during 2026. Kabuli chana exports surged 78% year-on-year to 1,76,389 tonnes during Apr–Feb 2026, while February exports alone jumped nearly 59%, reflecting sustained overseas buying interest. Reduced Australian chickpea shipments to India and Canadian exports below 2,000 tonnes further tightened import-side pressure, supporting domestic market fundamentals and improving medium-term price outlook.

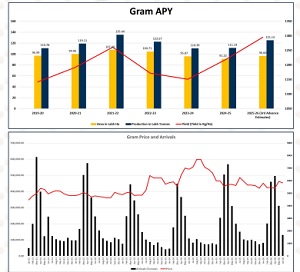

MSP Hike & Procurement Measures Boost Sentiment: Government policy measures continued providing strong support to domestic chana prices despite comfortable global supply availability. The government increased MSP by Rs.225 to Rs.5,875 per quintal and extended Maharashtra procurement quantity by 58,632 tonnes to 8,19,882 tonnes. Additionally, the 30% duty on yellow peas supported domestic consumption demand, although higher projected production at 117.92 lakh tonnes capped aggressive bullish expectations.

Weather Risks Vs Global Supply Pressure: Weather and supply-side developments continued creating mixed sentiment across the chana market. Heatwave risks across Northern India threatened standing crop productivity, while Red Sea geopolitical tensions raised freight costs and supported domestic prices. However, Australian chickpea exports at 1.36 million tonnes, port stocks of 3.14 lakh tonnes and expectations of higher Canadian carryover stocks continued maintaining pressure from abundant global supply conditions.

Technical Outlook: Technical indicators suggest improving medium-term structure despite broader supply-side pressure. Prices continue stabilizing after forming a strong base near lower support zones, while momentum indicators are gradually improving. As per technical outlook, buy-on-drop strategy remains favorable. Volatility expectations remain elevated, although improving structure and recovering momentum indicate potential continuation toward higher resistance zones if support areas continue sustaining

Highlights

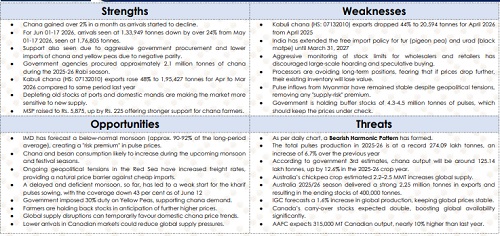

* Chana prices gained over 2% monthly as declining arrivals tightened physical market availability significantly.

* June arrivals dropped more than 24%, supporting sentiment through reduced near-term market supplies.

* Aggressive government procurement and lower import parity strengthened domestic chana price fundamentals considerably.

* Government agencies procured nearly 2.1 million tonnes, providing strong underlying market support levels.

* Kabuli chana exports surged 48% during FY2025-26, reflecting robust international demand conditions.

* Depleting old stocks across ports and mandis increased market sensitivity to fresh supplies.

* Higher MSP of ?5,875 per quintal strengthened farmer holding capacity and price support.

* Free import policy extension for tur and urad continues weighing on overall pulse sentiment.

* Stable pulse inflows from Myanmar eased supply concerns and reduced risk-premium pricing.

* Government buffer stocks exceeding 4.3 million tonnes could cap excessive upside movements.

* Processors remain cautious on long-term purchases amid concerns of potential inventory value erosion.

* Below-normal monsoon forecasts have introduced a weather-related risk premium into pulse markets.

* Delayed kharif pulse sowing and lower acreage may tighten future domestic supply prospects.

* 30% duty on yellow peas continues supporting domestic chana consumption and demand.

* Farmers in major producing states are holding stocks anticipating higher realizations ahead.

* Record domestic chana production and rising global supplies remain significant medium-term market headwinds.

* Expanding Australian and Canadian chickpea availability could limit sustained rallies in domestic prices

Conclusion

Price Performance: Chana prices gained over 2% during the month as arrivals declined sharply, tightening physical market availability. Arrivals for June 1–17 stood at 1,33,949 tonnes, down more than 24% from 1,76,805 tonnes recorded during May 1–17. Support also emerged from lower import parity and stronger domestic demand, though record production expectations continued to cap upside.

Arrivals & Government Procurement: Market sentiment remained supported by aggressive government procurement and declining arrivals. Government agencies procured approximately 2.1 million tonnes during the 2025-26 rabi season, while depleting stocks at ports and mandis increased sensitivity to fresh supplies. Higher MSP of Rs.5,875 per quintal further strengthened farmer holding capacity and provided a solid floor to prices.

Demand & Trade Dynamics: Demand fundamentals remained favorable as Kabuli chana exports increased 48% to 1,95,427 tonnes during FY2025-26. Additionally, the government’s 30% duty on yellow peas supported domestic chana consumption. However, free import policy extensions for tur and urad until March 2027, along with stable pulse inflows from Myanmar, reduced supply-risk premiums and tempered bullish sentiment.

Production & Global Supply Pressure: Despite near-term support, medium-term fundamentals remain challenging. Total pulses production is estimated at a record 274.09 lakh tonnes, up 6.7% YoY, while chana production is projected at 125.14 lakh tonnes, up 12.6%. Expanding Australian chickpea supplies of 2.2–2.5 MMT, higher Canadian output, and rising global production forecasts continue to weigh on long-term price prospects.

Technical Outlook: Technically, prices remain above key 50-day and 200-day moving averages, reflecting underlying strength. However, a bearish crossover on MACD and the formation of a Bearish Harmonic Pattern indicate weakening momentum. Volatility indicators suggest corrective pressure may emerge, with prices vulnerable to downside retracement despite supportive near-term fundamentals

Above views are of the author and not of the website kindly read disclaimer