Paddy Report As On 20th June 2026 by Amit Gupta, Kedia Advisory

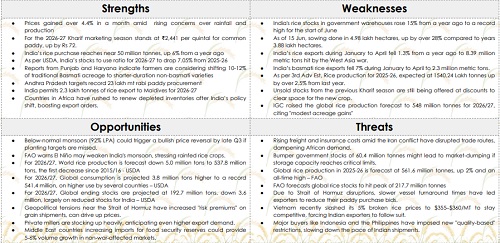

Price Performance: Paddy prices declined over 6% during the month amid export disruptions caused by the Middle East conflict, which delayed nearly 200,000 tonnes of basmati rice shipments. India’s rice export value also fell 6% in April due to rising freight and insurance costs of 25–30%. However, tightening global supply expectations and renewed African demand provided partial support.

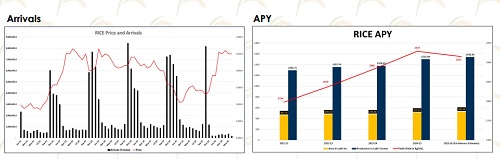

Domestic Supply & Stocks: India’s rice production for 2025-26 is estimated at 1239.28 lakh tonnes, around 1% higher YoY, reflecting favorable acreage and productivity. Rabi paddy acreage also increased 15.19% YoY, signaling abundant domestic supplies. Additionally, government stocks remain elevated at 60.4 million tonnes, raising risks of market dumping if storage capacities become critically stretched during the upcoming procurement cycle.

Global Demand & Trade Dynamics: Global rice fundamentals remain mixed as USDA projects 2026-27 world rice production lower by 5 million tonnes to 537.8 million tonnes, the first decline since 2015-16. Global consumption is projected at a record 541.4 million tonnes, while ending stocks may decline 3.6 million tonnes. However, Vietnam’s aggressive pricing and new import restrictions from Indonesia and Philippines continue pressuring Indian exports.

Weather & Export Risks: Below-normal monsoon expectations at 92% of LPA could trigger supply concerns if kharif sowing targets are missed later in the season. Heavy rains already damaged over 2 lakh hectares of crops in Maharashtra, while unseasonal rains affected Andhra Pradesh and Telangana. Simultaneously, geopolitical tensions around the Strait of Hormuz increased freight costs and disrupted vessel turnaround times, weakening export competitiveness.

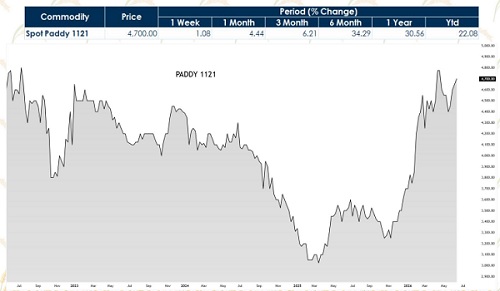

Technical Outlook: Technically, a bearish harmonic pattern has formed on the weekly chart, indicating continuation of corrective weakness. RSI and MACD structures remain negative, while elevated volatility signals sustained downside pressure. Prices are expected to remain under pressure below the resistance zone of 4850–5000. Immediate downside targets are seen near 4300–4200, while extended weakness could drag prices towards 4100 and 3960 levels.

Highlights

* Paddy prices gained over 4% monthly amid rising concerns regarding monsoon progress and production prospects.

* Government increased paddy MSP by ?72 to ?2,441 per quintal for 2026-27 season.

* India’s rice procurement approached 50 million tonnes, rising 6% from previous year levels.

* USDA projects India’s rice stock-to-use ratio declining over 7%, tightening future availability outlook.

* Farmers in Punjab and Haryana are shifting acreage from basmati to non-basmati varieties.

* Andhra Pradesh targets record rabi paddy procurement of 23 lakh tonnes, supporting demand.

* India approved 2.3 lakh tonnes rice exports to Maldives, boosting export market sentiment.

* African nations accelerated rice purchases after India’s policy shift, strengthening export order books.

* India retains dominant global rice export share, maintaining strong influence over international pricing.

* Government rice stocks surged 15% annually to record highs at the beginning of June.

* Paddy sowing increased over 28% year-on-year, indicating improved planting progress across regions.

* Middle East conflict disrupted rice shipments and reduced India’s export volumes during early 2026.

* Record rice production estimates above 154 million tonnes ensure comfortable domestic supply availability.

* Below-normal monsoon forecasts and El Niño concerns could support prices during later quarters.

* Global rice consumption is projected at record levels, exceeding production growth in 2026-27.

* Geopolitical tensions and higher freight costs continue raising risk premiums on rice shipments.

* Private millers are actively building inventories, anticipating stronger export demand and higher prices.

* Record global rice stocks and rising production may limit sustained upside in prices.

Conclusion

Price Performance: Paddy prices gained 4.14% during the month and 34.29% over six months, supported by concerns over monsoon progress and production prospects. The government increased MSP by Rs.72 to Rs.2,441 per quintal for the 2026-27 season, providing price support. However, record production estimates above 154 million tonnes and rising government stocks continue to limit aggressive upside potential.

Domestic Supply & Stocks: India’s rice production for 2025-26 is estimated at 1,239.28 lakh tonnes, around 1% higher YoY, while rabi paddy acreage increased 15.19% YoY, indicating ample domestic availability. Government rice stocks have surged to 60.4 million tonnes and were reported 15% higher annually, creating potential market-dumping risks if storage constraints intensify.

Global Demand & Trade Dynamics: Global rice fundamentals remain mixed. USDA projects 2026-27 world rice production at 537.8 million tonnes, down 5 million tonnes, while global consumption is expected to reach a record 541.4 million tonnes. Ending stocks are projected to decline by 3.6 million tonnes. Supporting sentiment, India approved 2.3 lakh tonnes of rice exports to Maldives and African nations accelerated purchases, although Vietnam’s aggressive pricing and new import restrictions from Indonesia and the Philippines continue pressuring exports.

Weather & Export Risks: Weather and geopolitical developments remain critical drivers. Below-normal monsoon expectations at 92% of LPA and El Niño concerns may threaten kharif production if sowing targets are missed. Heavy rains damaged more than 2 lakh hectares in Maharashtra, while geopolitical tensions around the Strait of Hormuz increased freight and insurance costs by disrupting trade routes.

Technical Outlook: Technically, paddy has formed a Bearish Harmonic Pattern on the weekly chart. RSI and MACD structures continue indicating negative momentum, while elevated volatility suggests sustained price swings. The market remains vulnerable below major resistance zones, and technical indicators favor corrective weakness. Although short-term rebounds may emerge, the prevailing structure continues to point toward downside risks as long as resistance levels remain intact.

Above views are of the author and not of the website kindly read disclaimer