Cables and Wires Sector Update :C&W Industry poised for continued outperformance by Motilal Oswal Financial Services Ltd

Higher growth visibility drives earnings upgrades

* The cables & wires (C&W) industry has emerged as a key beneficiary of the country’s ongoing infrastructure expansion and electrification drive. Demand is supported by multiple structural growth drivers, including power transmission and distribution, residential and commercial construction, railways, telecommunications, renewable energy, and industrial capex. This diversified demand base provides sustained growth visibility and reduces dependence on any single sector.

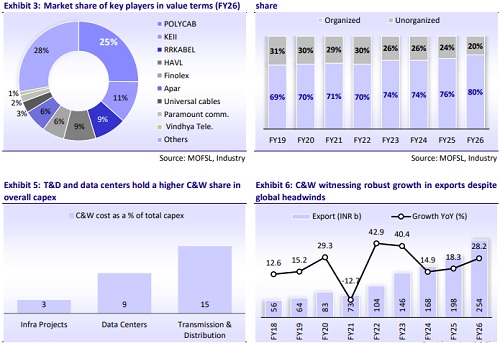

* The C&W industry expanded at a CAGR of 12.5% over FY22-26 to INR1.0t, with organized players delivering robust growth of ~17% over the same period. As a result, the share of organized players (%) increased to ~80% in FY26 from ~67% in FY22. Looking ahead, the industry is expected to sustain its strong growth trajectory, with demand projected to grow at approximately 1.5x-2.0x real GDP growth over the medium term. This is underpinned by the sector’s direct exposure to infrastructure development, urbanization, industrialization, and rising power consumption across the economy.

* Given the stronger revenue growth outlook, supported by capacity expansions, market share gains, and margin expansion, we raise our EPS estimates for POLYCAB by ~8% for FY27-28 (each), and for RRKABEL by ~11% for FY27-28 (each). We have largely maintained earnings for KEII and HAVL. Within our coverage universe, POLYCAB posted industry-leading growth of ~24%, followed by KEII/RRKABEL at ~21% (each) and HAVL’s at ~17% over FY22-26. We estimate POLYCAB to continue delivering industry-leading growth, with ~22% revenue CAGR over FY26-28, followed by RRKABEL and KEII at ~21% (each) and HAVL at ~14%.

Energy transition and grid investments to drive multi-year growth

* India’s energy transition remains a major long-term growth driver for the C&W industry. India added 57.5GW of generation capacity in FY26, with solar and wind accounting for ~76% /11% of additions, respectively. Total installed power capacity reached 533GW, with non-fossil fuel sources contributing over ~50% of installed capacity. Supported by sustained investments in solar, wind, battery storage, and related infrastructure, India continues to progress toward its target of achieving 500GW of non-fossil fuel power capacity by 2030.

* Renewable energy projects are inherently cable-intensive, requiring extensive cabling for power collection, transmission, and grid connectivity. As renewable capacity additions continue to accelerate, demand for specialized power and transmission cables is expected to increase significantly.

* Rising power demand and large-scale investments in transmission and distribution infrastructure provide an additional growth lever for the industry. India's per capita power consumption is projected to increase from 1,395 units in FY24 to 2,984 units by FY40, driving significant investments across the power value chain. The power T&D sector is expected to attract over INR9t of investments over the next seven years, while annual transmission line additions are projected to increase substantially by FY30E, with annual transmission line additions scaling 5x to 41,000 km

* Grid modernization initiatives are further supporting demand for specialized cables and conductors. According to the National Electricity Plan (NEP), over 191,000 ckm of transmission lines and 1,270 GVA of transformation capacity are planned to be added between FY23 and FY32. Additionally, initiatives such as the INR3.03t Revamped Distribution Sector Scheme (RDSS), the National Green Hydrogen Mission, smart metering programs, feeder separation projects, and smart-grid deployment are expected to drive sustained demand for cables used in efficient power transmission and renewable energy integration.

Rating upgrade to BUY for RRKABEL; maintain on POLYCAB (BUY) and KEII (BUY)

* We raise EPS estimates for POLYCAB by ~8% for FY27-28 (each), and for RRKABEL by ~11% for FY27-28 (each), given the stronger revenue growth outlook supported by capacity expansions, market share gain, and margin expansion. Meanwhile, we maintain earnings for KEII and HAVL.

* We estimate revenue/EBIT CAGR at ~21%/22% over FY26-28 for our coverage companies vs. revenue/EBIT CAGR of ~23%/24% posted over FY24-26. We project EBIT margins at 12.3%/12.7% in FY27/FY28 vs. 12.4% in FY26, driven by an increase in the scale of operations, higher contribution from power cables, and exports contribution.

* We upgrade RRKABEL to BUY from Neutral, considering the strong growth outlook and margin expansion, while we reiterate our BUY rating on POLYCAB and KEII. We continue to believe that the sector’s demand tailwinds will remain intact over the long term

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Automobiles Sector Update : MSIL/TMPV outperform in PVs, TVS in 2Ws, and TMCV in CVs by Moti...