Buy Zensar Tech Ltd for Target Rs.650 by Choice Institutional Equities

Steady Performance amid Weak Demand & Margin Headwinds

ZENT delivered a mixed Q4FY26, with underlying demand weakening. A key positive was mega deal win of USD 401.8 Mn (+123% QoQ), signalling robust pipeline traction and improving client confidence. While management expects near-term margin pressure in H1FY27 due to large deal transition costs, it has maintained its full-year margin guidance of 14–16%, indicating confidence in underlying operational levers. We remain structurally constructive on the longterm story, as ZENT continues to transition toward an AI-native enterprise, embedding AI across offerings and scaling capabilities such as Quality Intelligence and Agentic AI to expand its addressable market. However, we expect near-term headwinds to persist, driven by continued softness in TMT and HLS, client exits due to consolidation, and margin pressure from upfront investments and transition costs. We expect Revenue/EBIT/PAT CAGR of 8.7%/11.8%/11.4% over FY26–29E. Accordingly, while the long-term thesis remains intact, we moderate our near-term expectations and revise our target price to INR 650 (implied PE 15x) to reflect these transitory challenges. Maintain ‘BUY

Muted Revenue Growth; Strong Deal Pipeline and Stable Profitability

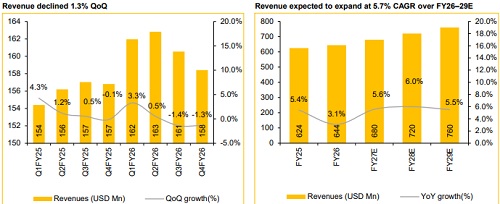

* In Q4FY26, ZENT posted revenue of USD 158.4 Mn, down 1.3% QoQ (vs CIE estimate of -1.9% QoQ). CC growth came in at -1.9% QoQ. In INR terms, revenue stood at INR 14,504 Mn, up 1.4% QoQ (vs CIE estimate of +0.6% QoQ). For the full year, revenue came in at USD 643.7 Mn, up 3.1% YoY, whereas in INR terms, it stood at INR 56,874, up 7.7% YoY.

* EBIT margin came in at 14.7% (vs CIE estimate of 15.3%) for Q4FY26, down 130 bps QoQ and, for FY26, it stood at 14.5%, up 100 bps YoY.

* PAT for the quarter stood at INR 2,106 Mn, up 5.4% QoQ (vs CIE estimate of +5.1% QoQ), whereas, for FY26, PAT stood at INR 7,746 Mn, up 19.2% YoY.

Robust Order Book; TMT Vertical Pressures Persist

ZENT’s reported record deal momentum with an all-time high quarterly order book of USD 401.8 Mn, up 123% QoQ. Even excluding the mega deal, order bookings remained strong at approximately USD 206 Mn for the quarter. Vertical-wise, BFS (+1.2%) was the top performer; whereas HLS (- 6.6%), TMT (-3.8%) and Manufacturing & Consumer Services (-3.9%) de-grew sequentially due to continuous pressure led by significant cost-cutting and insourcing. HLS is expected to remain flat in FY27 as the company ‘consolidated out’ of a couple of accounts. However, strong deal wins imply stabilisation in core verticals, with early signs of recovery, led by cost optimisation and transformation-led demand.

Margins Soft Near-term; Structural Stability Intact

EBIT margin came in at 14.7% for Q4FY26, down 130 bps QoQ and for FY26, it stood at 14.5%, up 97 bps YoY. The margin contraction was a sum of factors such as lower volumes due to fewer working days, reversal of leave utilisation benefits from Q3 increased SG&A costs, which were partially offset by a 1.2% positive forex impact. Margin pressure is anticipated to persist in the H1 of FY27 majorly due to upfront investments and transition costs for the mega deal. The management maintained their long-term guidance of mid-teens (14% to 16%) for the full year.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131