Buy AAVAS Financiers Ltd for the Target Rs. 1,500 By Prabhudas Lilladher Ltd

Quick Pointers

Expect disbursements to ramp up in Q4/ FY27

Potential rating upgrade to support NIM; stable asset quality

Over the past three years, AAVAS has faced management changes, promoter stake sale, and regulatory headwinds, which have now largely subsided. Expect disbursements to pick up driven by branch expansion, CSC scale-up and RRO model. Company expects AUM growth of 18%/ 20% in FY27/ FY28E; we build 17%/ 18% as execution in non-RJ markets is key. Potential credit rating upgrade by July-26 is likely to support NIMs. Opex is expected to be elevated in FY27 due to new branch additions; credit cost is expected to remain benign at 15-16bps. We roll-forward to FY28E with a TP of Rs 1,500 (1.8x FY28E P/ABV). Stock has corrected 11.5% over the past month; maintain BUY on sustainable growth and margin outlook.

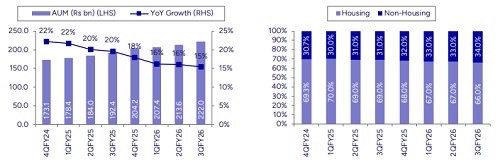

Expect AUM growth of 18% in FY27E: AAVAS expects disbursement run-rate to pick up in Q4FY26 with a target of ~Rs 23bn (vs. Rs 17.2 bn in Q3FY26) aided by improved salesforce and tech integration. It is targeting ~ Rs 70bn of disbursements in FY27 with an AUM growth of ~18% in FY27E and ~20% in FY28E. Growth is expected to be driven by i) branch expansion (~50 additions in FY27, adding Rs 1–1.5bn incremental business), scaling up of the CSC (Common Service Centre) channel (from ~Rs 4bn in FY26 to ~?11bn in FY27) and steady contribution from RROs (~Rs0.5–0.6bn disbursements at ~14.5% yields). On the geography front, core markets such as RJ continue to deliver 20–25% growth with pristine asset quality, while previously underperforming states like KA, MH and GJ are expected to recover, supported by management bandwidth. Additionally, it plans to expand into regions such as TN & UP (where branch presence remains lower vs. peers) which provides significant headroom for growth.

CoF to improve in FY27; opex elevated: Management indicated a stable CoF in Q1FY27 and anticipates a credit rating upgrade by July-26, cushioning margins. On the opex side, it guided for a Cost/Income ratio of <40% in FY27 and ~35% over the medium term. Asset quality outlook remains stable, with a cautious stance in MP (limited to 5–10% growth) given its historically volatile nature, while core markets continue to perform well. Credit cost is expected to remain benign at ~15–16bps. While we expect credit cost to be in-line, we build a higher opex (C/I ratio of ~43% over FY26-28E), factoring in new branch additions.

Please refer disclaimer at Report

SEBI Registration number is INH000000933