Buy Park Medi World Ltd for the Target Rs.320 by Choice Institutional Equities

Capacity expansion and superior case mix drive growth:

PARKHOSP's debtfree balance sheet funding capacity expansion at INR 34 lakhs/bed, creates a structurally differentiated, self-compounding growth engine with multi-year earnings visibility. The growth will be driven by aggressive capacity expansion with low capex per bed, a shift towards a higher-end case mix, optimisation of ALOS, improvement in payor mix and gains from revised CGHS rates. We expect Revenue/EBITDA/PAT to expand at a CAGR of 26.0%/26.1%/31.6% over FY26–29E.

View and valuation:

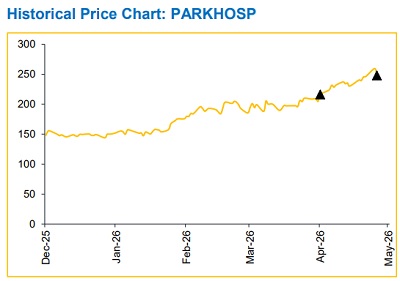

We value the company at 18x EV/EBITDA on FY28E and hence maintain our ‘BUY’ rating with a target price of INR 320.

Results were in line with estimate, achieved highest-ever EBITDA margin

* Revenue came in at INR 4.6 Bn (vs. CIE estimate: INR 4.6 Bn), up 30.1% YoY and 12.3% QoQ.

* EBITDA came in at INR 1.3 Bn (vs. CIE estimate: INR 1.2 Bn), up by 44.0% YoY and 28.1% QoQ. EBITDA margin at 27.7% (vs. CIE estimate of 25.7%), significantly improving by 268 bps YoY and 342 bps QoQ.

* PAT came in at INR 0.7 Bn (vs. CIE estimate: INR 0.7 Bn), up 58.1% YoY and 39.6% QoQ, with a PAT margin of 15.4%.

Aggressive capacity expansion from 3,610 to 10,000 beds with lowest capex per bed:

PARKHOSP is driving one of India’s most capital-efficient hospital expansions, growing from 3,610 beds in FY26 to 5,460 by FY28 and targeting over 10,000 beds in the next five years, all funded through internal accruals with zero equity dilution. Its cluster-led expansion model achieves industryleading capex efficiency at ~INR 34 lakh per bed vs INR 80–100 lakh for greenfield peers, while maintaining high clinical standards. Strategic acquisitions of distressed assets and an optimised bed mix further strengthen scalability, profitability and long-term compounding potential.

Shift towards high-end case mix, supported by strong infrastructure:

PARKHOSP is steadily shifting toward a higher-acuity, high-margin case mix, supported by advanced robotic surgery infrastructure and a scalable full-time doctor model. With robotic utilisation still at early-stage levels, significant operating leverage and margin expansion remain ahead. Improving ALOS and rising ARPOB reflect stronger clinical efficiency, while standardised systems across hospitals position the company for sustained long-term growth.

Benefit from revised CGHS rate and improving payor mix:

PARKHOSP benefits from a strong government payor mix, creating stable demand and limited competitive pressure. The recent 12–15% CGHS rate hike is expected to drive a meaningful revenue and EBITDA uplift as revisions flow through ECHS, Railways and state schemes by H2FY27. At the same time, a gradual shift toward a higher private-pay mix should improve collections, strengthen cash flows and support earnings growth.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131