Buy Westlife Development Ltd for the Target Rs. 750 by Motilal Oswal Financial Services Ltd

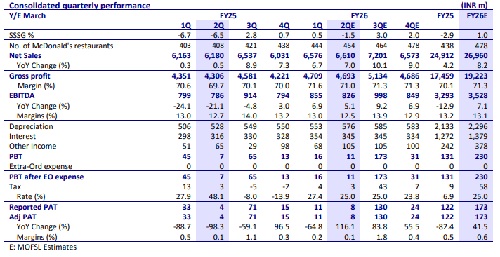

* We expect 7% revenue growth, led by 11% store growth (10 store addition). Same-store sales expected to decline 1-2% on a weak base. There is no material change in demand environment; remains subdued. Extended rainfalls and shift in festivities further impacted the already soft demand.

* ADS is expected to decline 4% YoY to INR162k.

* Gross margin is expected to improve 130bp at 71%. Operating margin expected to decline marginally 20bp YoY to 12.5% primarily due to operating deleverage.

* We model EBITDA Pre-Ind AS margins at 7.2% for 2QFY26, 50 bp down YoY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412